Volume

4, Number 1, 2017, 1–16 journal homepage:

region.ersa.org

Volume

4, Number 1, 2017, 1–16 journal homepage:

region.ersa.orgDOI: 10.18335/region.v4i1.95

Does the increase in house prices influence the creation of business startups? The case of Sweden

1 Royal Institute of Technology, Stockholm, Sweden (email: bjorn.berggren@abe.kth.se)2 Royal Institute of Technology, Stockholm, Sweden (email: andreas.fili@abe.kth.se)

3 Royal Institute of Technology, Stockholm, Sweden (email: mats.wilhelmsson@abe.kth.se) Received: 22 September 2015/Accepted: 22 November 2016

Abstract. Entrepreneurs are at the core of economic development in that they start new businesses or make existing firms grow. To fulfill this important role, entrepreneurs need access to financing. Owing to information asymmetry and the relatively high risk associated with business startups, many financiers shy away from engaging in relationships with firms during the early stages of their development. Based on the existing body of knowledge on the financing of entrepreneurship, we know that insider finance is of paramount importance in the early stages of firms’ development. We expand this knowledge base by analyzing the influence of house prices on business startups across municipalities in Sweden. In our analysis, we include data from all municipalities in Sweden. Our data on house prices and control variables are collected in period one, and our data on the frequency of startups are collected in period two. We find that rising house prices in a municipality lead to a higher frequency of startups. In our spatial Durbin model, we find that a 1% increase in house prices leads to around 0.15% increase in startups. Our findings are in line with the limited international research that has been previously conducted, and therefore, our study might make a small but vital addition to this growing body of knowledge within the area of entrepreneurship and regional development.

JEL classification: R11, R31, M13

Key words: Business startups, entrepreneurship, financing, house prices, mortgages

1 Introduction

In the late 1970s, scholars concluded that small and medium-sized enterprises (SMEs) create the majority of new jobs in the U.S. economy (Birch 1979). These findings spurred great interest in research on the employment contribution of SMEs worldwide, with scholars concluding that SMEs contribute to 70% to 90% of all new jobs that are created (Davidsson et al. 1995, Armington, Acs 2002, Santarelli, Tran 2012). Previous research has shown that in addition to playing a vital role in the creation of employment opportunity, startups and SMEs are involved in creating industrial renewal, export income, and innovation (Halilem et al. 2012, Agostini et al. 2015, Love, Roper 2015), as well as acting as a dynamic influence to lagging areas (Keeble 1997, Gordon, McCann 2005, Doh, Kim 2014)(Keeble 1997, Gordon, McCann 2005, Doh, Kim 2014). Therefore, governments in most nations have developed different types of programs to support SMEs and startups (Bateman 2000, Perren, Jennings 2005).

To fulfill the role of creators of new employment, export income, and innovations, new firms must secure access to financial resources (Harding, Cowling 2006, Atherton 2012). Previous research has shown that the most important source of finance for newly started firms is insider finance (Cassar 2004, Gregory et al. 2005, Robb, Robinson 2014). Insider finance includes the personal funds of the founder: personal savings, home mortgage, and credit cards (Storey, Greene 2013). This implies that a booming housing market would enhance the ability of entrepreneurs to increase their home mortgage, or at least enhance their ability to take on new loans by virtue of the increase in collateral they can offer the bank, and, thus, finance their newly started firms – a causality that has been established by Jin et al. (2012).

In this paper, we build on the findings of Jin et al. (2012) and use Sweden as our empirical case. More specifically, we attempt to identify and estimate an empirical model of the relationship between business startups and house prices in all 290 Swedish municipalities.

The remainder of the paper is organized as follows: In section 2, we present some key findings from previous studies on the financing of entrepreneurial ventures and the relationship between house prices and business startups. Next, we present the empirical model in Section 3 and describe our data in Section 4. We then present our results in Section 5 and conclude the paper with a discussion of our findings in Section 6.

2 Theoretical points of departure

Financing entrepreneurship and business startups have received a great deal of attention from researchers and policymakers for over 100 years (see MacMillan 1931). According to conventional wisdom, small and medium-sized firms have problems accessing finance at reasonable terms (see Storey, Greene 2013). Whether SMEs are, in fact, subject to credit rationing is a question that has been asked in numerous research studies but is one that remains unanswered. A consensus, however, has been reached regarding the dependency of entrepreneurial ventures on insider finance in their earlier stages of development as well as regarding the higher degree of financial constraints experienced by SMEs in comparison to larger organizations (Cassar 2004, Revest, Sapio 2012). As a consequence, there has been considerable research interest in the financing of new firms. Three major theories have been used to illustrate financing patterns: life-cycle theory, pecking order theory, and agency theory (Berger, Udell 1998, Johnsen, McMahon 2005). The first two theories focus on the perspective of the firm that receives financing, whereas agency theory takes the perspective of the investor that provides financing.

2.1 Different perspectives on the financing of entrepreneurial ventures

Life-cycle theory suggests that firms, depending on what stage of development they have reached, follow similar financing patterns (Weston, Brigham 1981). Research has revealed that firms in certain stages of development seek certain types of financing and that firms have similar financing needs and financing behavior – no matter the cultural differences across countries (cf. Psillaki, Daskalakis 2009). Studies from all over the world – including Europe (Psillaki, Daskalakis 2009), China (Newman et al. 2012), and Africa (Abor, Biekpe 2009) – have provided support for this perspective.

Pecking order theory is concerned with explaining why firms do not always prefer the source of financing with the lowest interest rate. Research has shown that there seems to be a stable preference order – a pecking order – whereby different sources of financing are ranked (Donaldson 1984, Myers 1984). In essence, the theory states that there is a general mistrust of outsiders: the more a firm is likely to lose control to external financiers, the less likely it is to submit to that type of financing. Internally generated funds are preferred to bank loans, which in turn are preferred to new equity. Although initial studies were conducted in large companies, several studies have shown that the pecking order framework is a fruitful approach to studying financial decision-making in small firms as well (Vanacker, Manigart 2010, Degryse et al. 2012, Alon, Rottig 2013) and that SMEs follow a financial pecking order when they seek external financing (Berggren et al. 2000). Like life-cycle theory, pecking order theory is a well-established theory, and numerous studies have found support for it (cf. Davidsson et al. 2009, Mac an Bhaird, Lucey 2011).

Whereas both life-cycle theory and pecking order theory focus on the perspective of the firm, agency theory takes the perspective of the investor. Agency theory models entrepreneurial finance in terms of contracts between a principal and an agent, where the goals of the two parties diverge (Jensen, Meckling 1976). Thus, as soon as the investor has supplied funding, the firm will try to use those resources for personal gains instead of for the benefit of the investor. The fact that these goals differ implies that once the funding has been supplied, the investor needs to ensure – through monitoring and control – that the funds are used properly (Ross 1973).

2.2 Implications of the financial perspectives for entrepreneurial finance

The major explanatory construct in pecking order theory is the notion of control aversion. The pecking order theory predicts that banks will be preferred to new shareholders. However, this notion is also quite clearly linked to life-cycle theory, in that control aversion is especially prevalent among young firms: overcoming control aversion is partly a matter of reaching maturity in dealing with business associates, financiers, and presumptive owners. Because control aversion is prevalent among young firms, they will often act in accordance with pecking order theory by contacting banks, rather than new owners (Howorth 2001, Paul et al. 2007).

The bank, in line with agency theory, will also demand some measures of control, primarily through collateral provided personally by the founder(s). Thus, the very foundational assumption of agency theory leads to a strong focus on control, which was initially the reason for the firm’s decision not to seek other sources of financing. The lazy bank hypothesis states that collateral is not an effective measure against bankruptcy, but merely an easy way of handling SMEs (Manove et al. 2001). Still, as the bank retains the right to cancel a loan at any time, collateral, performance data and legitimacy represent significant obstacles to new enterprises (Bracke et al. 2013, De Clercq et al. 2013, Ramlall 2014). Because of the pivotal role of collateral, the size of the collateral also proves to be important. Being able to offer a large portion of valuable collateral to the bank should mean more access to financing.

Most young firms have nominal collateral and credibility to offer the bank: they are not as transparent as older, larger firms (Robb, Robinson 2014). Moreover, service firms have fewer tangible assets (machinery and inventory) to offer as collateral for loans than do manufacturing firms. Instead, collateral is found in the personal property of the founder and, therefore, main sources of collateral are the houses of the founders’ (Chaney et al. 2012).

2.3 A model of higher house prices leading to an increase in business starts

Previous research shows that collateral is important for entrepreneurial activity. By using variations in house prices, Schmalz et al. (2013) provide evidence that in regions with house price appreciation homeowners are more likely to start a business; and the firms started by homeowners are larger than those started by renters. That is, collateral matters. Furthermore, Adelino et al. (2015) show, based on aggregated county data for the period 1998-2010, that regions with larger rises in house prices experienced stronger growth in employment in small firms, especially in industries with a limited need for capital.

The model is explained theoretically in the following way. First, higher house prices mean that nascent entrepreneurs have more collateral to offer to the bank when they apply for a loan to start the business (cf. Bernanke et al. 1999, Greenspan, Kennedy 2008, Jin et al. 2012, Bracke et al. 2013). This implies that banks can grant more loans to small businesses based on the fact that there is more private collateral on the part of the owner-founder of the firm. The model is part of an argument that claims that entrepreneurs suffer from a lack of funding (cf. MacMillan 1931, Stiglitz, Weiss 1981) and that sudden financial gains – “windfall gains” – have a positive effect on the number of business starts (Schäfer et al. 2011).

A number of papers lend support to this model. In their examination of the number of value added tax (VAT) registrations in the United Kingdom as well as other kinds of aggregate data, Black et al. (1996) found evidence that collateral availability does have a strong influence on firm formation and dissolution. By contrast, Hurst, Lusardi (2004) found no support for this hypothesis except in the very richest segment of households. Thus, they conclude that there is no general link between collateral and business starts. Robson (1996) compares his results explicitly with those of Black et al. (1996) from the same year and also in the United Kingdom. Although Robson (1996) finds no support for a link between high house prices and an increase in business starts, he states that housing wealth does appear to have a positive effect on entrepreneurship, in that it helps reduce the regional rate of deregistration from VAT.

This implies that an increase in house prices would equal an increase in the pool of liquidity available to entrepreneurs, which translates into a larger number of business starts in a certain region. According to this logic, a causal link may exist between a rise in house prices and the number of businesses started in a region as a result of greater access to collateral. Thus, our null hypothesis is formulated as follows:

There is a positive relationship between rising house prices and the number of business starts in a region.

3 Empirical model

To test our hypothesis that housing market conditions play an important role in explaining new firm formation, we estimate a model where the number of new firms per capita for the period 2007-2014 across Sweden is related to a number of determinants. Of main interest here is the relationship between new firm formation and housing price growth.

Two major problems may arise in this type of regional model. The first problem involves the issue of endogenous determinants. Because house price appreciation facilitates lending and, ultimately, increases entrepreneurial activity and economic growth, higher economic activity might result in more lending and higher house prices. That is to say, the relationship between house price appreciation and formation of new business startups is bidirectional (Iacoviello 2005, Adelino et al. 2015). The second problem involves the issue of spatial dependence. Both problems are connected to the question of how to interpret the estimated relationships as causality and not merely as correlations. That is, the empirical challenge is to identify the causal direction of the house price growth effect.

We avoid these potential problems by estimating a model using determinants in the preceding period (2007) when explaining the variation in firm formation in the subsequent period (2007-2014). In contrast to Binet, Facchini (2015), we estimate three types of spatial autoregressive models, a spatial lagged model and a spatial error model, as a means to control spatial dependence. We also estimate a spatial Durbin model in order to analyze if it could be simplified to a spatial error or lag model. Five different spatial weight matrices are tested. Two nearest neighbor, two inverse distance based and, finally, a spatial contiguity matrix. The distance is estimated using the centroid coordinates of the labor market.

Our approach has been used recently by Andersson et al. (2014), and earlier by Armington, Acs (2002). Our identification strategy is to relate the change in the number of startups in a region with the change and level of house prices in the previous period. That is, lagged house prices can have an effect on startups in a later period, but it is unlikely that startups in the future have an effect on house prices in a previous period (cf. Balasubramanyan, Coulson 2013).

New firm formation per capita varies to a great extent across municipalities in Sweden for the period 2007-2014. We use five different types of determinants to explain this variation, namely, (a) establishment structure, (b) labor market conditions, (c) human capital, (d) income, and (e) housing market conditions.

We use establishment size, measured as 2007 employment divided by the number of establishments in 2007, as a proxy for the structure of the industry in the region (see Armington, Acs 2002). The expected relationship is negative, as larger average establishment size should be negatively related to regional startups rates (Armington, Acs 2002).

Different measures are used here to measure labor market conditions. Both measures, number of employees in 2007 and unemployment rate in 2007, are included in the model. Number of employees measures the size of the market and is used instead of population (Binet, Facchini 2015) or number of households (Adelino et al. 2015) as a measure of the market size. It is a measure that captures some of the agglomeration effects observed in the literature (see Acs et al. 1994). One of the most important determinants used in previous research is the unemployment rate (see Armington, Acs 2002) as it was suggested that unemployed workers were more likely to start new firms. The unemployment rate is also used in more recent research (Adelino et al. 2015, Binet, Facchini 2015). The third labor market indicator we use is the self-employment rate in 2007. This measure of entrepreneurial culture (Johannisson 1984), has also been used in research by Armington, Acs (2002).

We also include a variable measuring the percentage of the population that was born outside of Sweden in 2007. Lee et al. (2004) used this diversity index, which they labeled the “Melting Pot Index.” The hypothesis is that a positive relationship exists between this index and new firm formation. The argument is that “immigrants lack skills, resources, and networks” and, therefore, tend to be self-employed and to start new companies to a greater extent than nonimmigrants. Migration data were also used by Adelino et al. (2015).

As a measure of human capital, we use the rate of university degree completion in the population in 2007. This measure is a proxy for the level of skill and knowledge in the regional economy (see Armington, Acs 2002, and, more recently, Adelino et al. 2015, Binet, Facchini 2015). The relationship between the rate of university degree completion in the population and new firm formation is expected to be positive.

Income is measured as the average annual regional income level in 2007 and is hypothesized to have a positive relationship with new firm formation in the subsequent 2007-2014 period. Based on the argument of Binet, Facchini (2015) that a high regional income level broadens the market size and, therefore, increases the number of opportunities for new firms, we would expect to observe more business startups in regions with higher regional income levels. We have also tested the change in annual income, but the empirical results suggest that it is not related to the number of new firms per capita. The level of income seems to be more important.

The housing market is included with two different measures. The first variable measures the annual growth in the seven years preceding 2007, that is, 2000-2006. The same type of measure is used by Schmalz et al. (2013) even though they use individual data. We also include a measure indicating whether the regional house price level in 2007 is above the average house price level.

4 Data

We use data on startups in Sweden from the period 2007 to 2014. The data are aggregated and based on all 290 municipalities in Sweden. The dependent variable is the change in the number of startups for the period 2007-2014. The independent variables all measured in 2007 are: human capital measured as the proportion with a university degree, income, employment, unemployment, and accessibility in the municipality as well as the change in house prices in the seven years preceding 2007 (2001-2007) and the house price level in 2007. Some descriptive statistics of the data are shown in Table 1.

|

Variable | Abbre- |

Period |

Average | Standard |

| viation | deviation | |||

| New firms per capita | New | 2007–2014 | 0.0505 | 0.0142 |

| University degree (%) | Univ | 2007 | 0.229 | 0.078 |

| High house prices (%) | High-Hp | 2007 | 0.33 | 0.47 |

| Change house price (%) | Dhp | 2001–2007 | 0.6926 | 0.3216 |

| Self-employment (%) | Self | 2007 | 9.7391 | 2.4726 |

| Employment | Emp | 2007 | 15,203 | 30,722 |

| Establishment size | Estab | 2007 | 8.4618 | 1.7561 |

| Income (SEK 000) | Inc | 2007 | 210.426 | 18.208 |

| Unemployment (%) | Unemp | 2007 | 6.6398 | 1.9628 |

| Immigration outside EU/EFTA (%) | Inm | 2007 | 4.6474 | 3.3232 |

| Stockholm (%) | Sthlm | 2007 | 0.1211 | 0.3268 |

In Table 1 we see that the average number of new firms per capita for the period is 0.05 (standard deviation: 0.01), which is equal to 5 new firms per 100 inhabitants. Almost 23% of the population has a university degree; the variation across the labor market is, however, substantial. House price appreciation is measured for the period 2001-2007. The average house price change is positive and equal to almost 0.7% (standard deviation: 0.3). Around one third of households in the labor markets have house prices that are higher than the average house prices. The average size of the labor markets, measured as the number of employees, is only 15,000 persons but the variation is considerable (standard deviation: 30,000 persons). The average unemployment rate is 6.6% with a variation of 2%. We measure the business set up in terms of establishment size. The average number of employees per establishment is equal to 8 persons (standard deviation: 1.7 persons). The entrepreneurial climate is measured with the self-employed variable. The average rate of self-employed is 9.7% with a variation of 2.5%. The number of immigrants as a percentage of the population is 4.6%, but the variation is substantial across the labor markets. Around 12% of the population lives in the labor market of Stockholm (the capital of Sweden). The correlation coefficients are shown in Table 2.

| New | Univ | High-hp | Dhp | Self | Emp | Estab | Inc | Unemp | Inm | |

| New | 1 | |||||||||

| Univ | 0.63* | 1 | ||||||||

| High-Hp | 0.71* | 0.74* | 1 | |||||||

| Dhp | 0.62* | 0.51* | 0.59* | 1 | ||||||

| Self | 0.28* | -0.23* | -0.12* | 0.03 | 1 | |||||

| Emp | 0.49* | 0.74* | 0.61* | 0.48* | -0.42* | 1 | ||||

| Estab | -0.11 | 0.34* | 0.26* | 0.14* | -0.85* | 0.45* | 1 | |||

| Inc | 0.34* | 0.66* | 0.66* | 0.62* | -0.42* | 0.57* | 0.63* | 1 | ||

| Unemp | -0.32* | -0.26* | -0.35* | -0.37* | -0.17* | -0.16* | -0.09* | -0.50* | 1 | |

| Inm | 0.22* | 0.38* | 0.41* | 0.29* | -0.47* | 0.30* | 0.47* | 0.39* | -0.25* | 1 |

The correlations between the dependent variable (New) and the independent variables are strong in most cases. The highest correlation among the dependent variable and an independent variable is between new firms and high house prices, indicating the importance of house prices as a channel of financing for startups. However, we can also observe high correlations between high house prices and high proportion with a university degree and between high house prices and high levels of income, with university degree and income being positively correlated with startups. The house price appreciation for 2001-2007 is positively correlated with new firm formation for 2007-2014. We also notice that the variable ‘employees per establishment’ and the self-employed variable are highly negatively correlated, indicating that it can be difficult to differentiate the effects in the empirical model. All correlations are statistically significant on a 5% level. In Section 5, we present the results from our empirical model in which we relate new firm formation per capita to all the determinants presented here.

4.1 Entrepreneurship in Sweden

Before we present and analyze the findings of our empirical model, we will present some of the key characteristics of startups within the Swedish economy. The number of startups in Sweden has increased over the past 20 years. Between 1994 and 2003, there were 34,000-39,000 startups per year, but in 2014 that number had increased to more than 71,000 startups per year (Statistics Sweden 2015). Two of the major reasons for the increased number of startups are simplified rules for incorporating a business and reduced capital requirements for limited liability companies. The number of bankruptcies has been relatively stable over the past ten years and in 2014 6,000 Swedish firms filed for bankruptcy (Statistics Sweden 2015).

In comparison with other European countries, the number of nascent entrepreneurs in Sweden is relatively low (GEM 2012). One reason for the relatively low levels of startups in the Swedish economy, in comparison with other nations, is lack of entrepreneurial spirit owing to a tradition of large enterprises within the Swedish economy. Instead it seems as though most entrepreneurial skills are distributed among established firms, a phenomenon that has been labeled intrapreneurship (GEM 2012). Even though relatively few firms are started each year in Sweden, the firms that do start have a higher survival rate than firms started in comparable countries (Andersson, Klepper 2013). Regarding industries, most startups are within the retailing and services industries. In 2014, more than 80% of all new firms were started in these two industries.

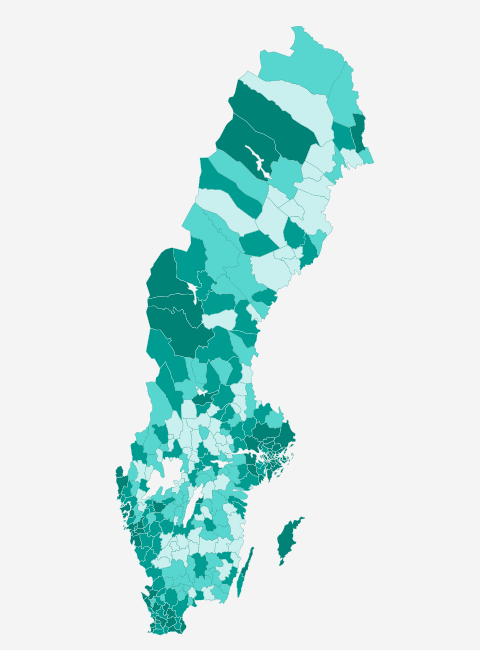

In Sweden, there are relatively large regional differences in startup frequency, see Figure 1. Among the hotspots for startups, as well as being the most dynamic regions, are the three metropolitan areas of Stockholm, Gothenburg and Malmo. We can also find some examples of municipalities outside these regions with relatively high frequencies of startups. Among these are municipalities on the border to Norway, as well as various regional centers where universities, hospitals, and other governmental agencies and institutions are located.

Source: Arena for Growth (2015)

5 Empirical results

Our main hypothesis is that the growth in house prices play a major role in explaining subsequent variation in new firms per capita. However, we also test the hypothesis that business set up, labor market conditions, human capital, and entrepreneurial climate play equally important roles when it comes to new firm formation. We test these hypotheses using a regression model where the dependent variable is the number of new firms per capita for the period 2007-2014. The independent variables used are those discussed in the previous section.

Tables 3-5 show the results from the ordinary least squares (OLS) estimation as well as from three types of spatial econometric models: the SAR-model (spatial autoregressive model), the SEM-model (spatial error model), and the spatial Durbin model (SDM).

For model comparison and selection of weight matrix we are following a specific-to-general test procedure proposed by Elhorst (2010). First we estimate an OLS and thereafter, using LM-tests (Anselin 1988, Anselin et al. 1996), testing for spatial dependency. If the LM-tests on OLS-residuals are significant, then SDM is estimated. If these LM-tests suggest that the SEM is the best spatial model, the log likelihood ratio test (LR-test) is used in order to test the convenience of SDM against SEM and SAR.

The next step is to select the spatial weight matrix. We are using three different types of weight matrices: nearest neighbor-based, distance-based and contiguity-based spatial matrix (discussed in for example Chasco 2013). All of them have been used in the spatial econometric literature (Elhorst 2010). Our selection of weight matrix is based on mobility pattern between municipalities. For example, contiguity and inverse distance have been used in Mendiola et al. (2015). We are using 2 and 10 nearest neighbor and 50 and 100 kilometers cut-off for the inverse distance matrix. The choice is somewhat arbitrary1 . However, as Elhorst (2010) says, the wrong choice of the spatial weight matrix can distort the estimates, but “the probability that this really happens is small if spatial dependence is strong” (Elhorst 2010). LeSage, Pace (2014) call the belief that the estimates are sensitive for the choice of spatial weight matrix “the biggest myth in spatial econometrics”. LeSage, Pace (2009), Stakhovych, Bijmolt (2009), and Halleck Vega, Elhorst (2013) are all in favor of using goodness-of-fit measures to discriminate among different spatial matrix specifications as there are no clear theoretical reasons for any specific form. We are using the most widely used log-likelihood value in order to differentiate between spatial weight matrices (Elhorst 2010). In order to test for the robustness of our coefficient estimates, we are analyzing the coefficients in the final spatial model specification using all the different spatial weight matrices.

As stated earlier, we are estimating the spatial Durbin model in order to test the hypothesis if this more general specification can be simplified with a spatial error (SEM) and/or autoregressive (lag) model (SAR). Here we are using the LR-test.

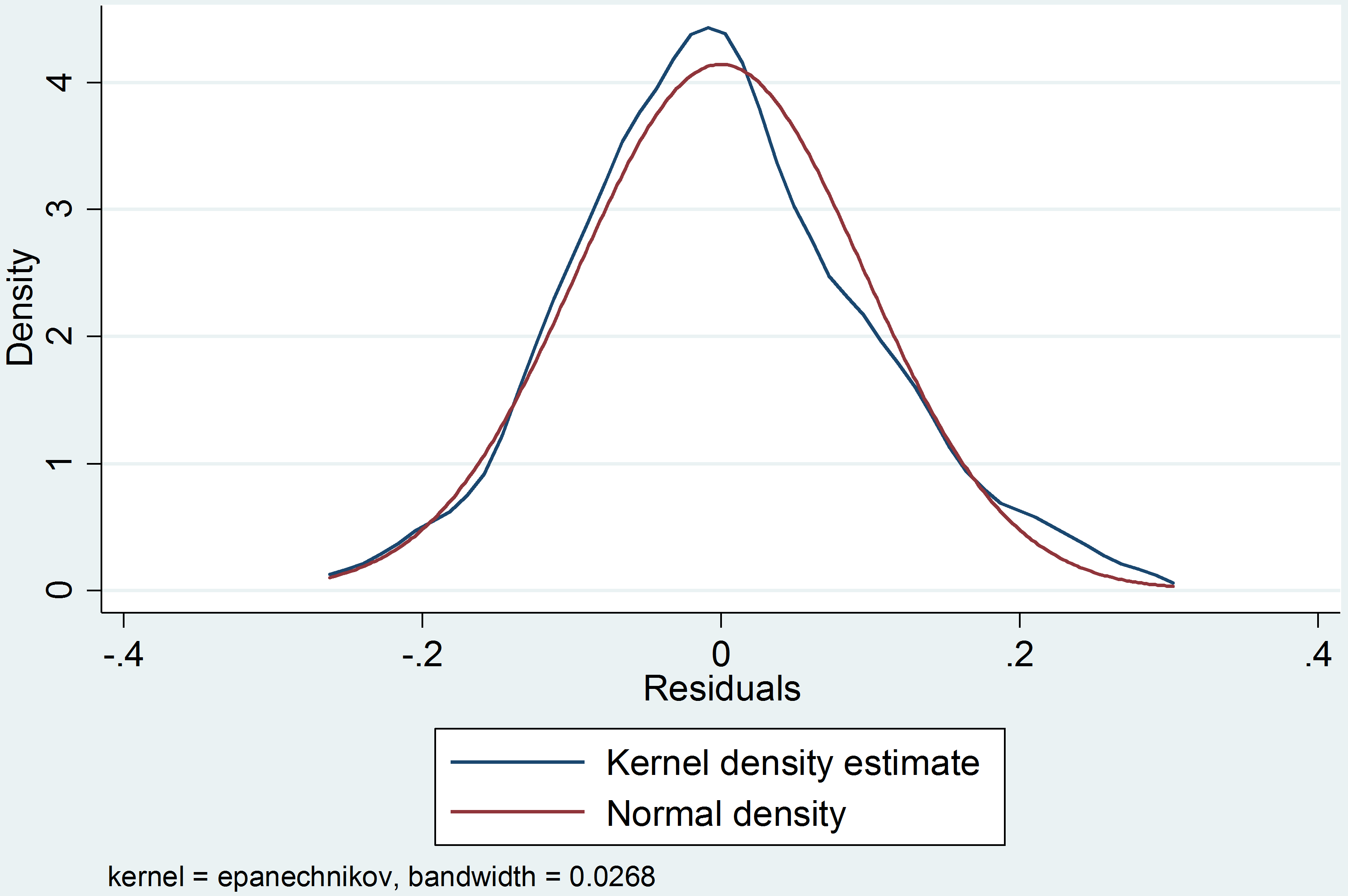

Table 3 shows the result from OLS. We are also testing for normality (Jarque-Bera), heteroscedasticity (Breusch-Pagan/Cook-Weisberg) and multicollinearity (Variance-of-inflation, VIF).

| Model 1 (OLS) | ||||||

| Coefficient | t value | VIF

| ||||

| High house prices | 0. | 1244 | 6. | 22 | 3. | 04 |

| Change in house prices | 0. | 1944 | 7. | 04 | 2. | 01 |

| Human capital | 0. | 1795 | 3. | 64 | 4. | 54 |

| Establishments | -0. | 1809 | -2. | 51 | 7. | 06 |

| Self-employed | 0. | 3136 | 5. | 71 | 6. | 94 |

| Employment | 0. | 0271 | 2. | 01 | 3. | 71 |

| Income | 0. | 4419 | 2. | 5 | 4. | 96 |

| Unemployment | 0. | 0978 | 3. | 08 | 2. | 28 |

| In-migration | 0. | 0217 | 1. | 44 | 2. | 25 |

| Stockholm | 0. | 1577 | 6. | 87 | 1. | 9 |

| Constant | -6. | 0839 | -5. | 97 | ||

| R2 | 0. | 832 | ||||

| R2-adjusted | 0. | 826 | ||||

| Jarque-Bera test (Prob >z) | 0. | 145 | ||||

| Breusch-Pagan/Cook-Weisberg test | 0. | 007 | ||||

| (Prob >chi2) | ||||||

| Observations | 289 | |||||

Around 83% of the variation in the total number of startups per capita between 2007 and 2014 can be explained by business set up, labor market conditions, and entrepreneurial climate, as well as by income and house price appreciation. The R2 value is considerably higher than that reported by Lee et al. (2004), for example, but is of the same magnitude as reported by Armington, Acs (2002). All coefficients have the expected signs and are statistically significant on a 95% level. The t ratios are calculated using White heteroscedasticity-robust standard deviations as the Breusch-Pagan/Cook-Weisberg test shows presence of heteroscedasticity. The Jarque-Bera test shows that residuals are normally distributed, that is, Maximum Likelihood (ML) is a suitable estimation method of the spatial error and spatial lag models. See also Figure 2 where the kernel density estimate is compared to the normal distribution. In the OLS model, we also present the variance of influence (VIF) so as to analyze potential multicollinearity issues. High correlation among the independent variables does not seem to create a problem of multicollinearity as VIF values are below 10.

Testing for spatial dependence (Moran’s I and the LM-tests with different spatial weight matrices) reveals that we do have a problem with spatial autocorrelation and/or spatial heteroscedasticity (Wilhelmsson 2002). Table 4 shows the results of the diagnostic tests for spatial dependence in OLS regression. Five different weight matrices are tested: two nearest neighbor (2 and 10), different inverse-distances based matrices with different cut-offs (50 and 200 kilometers) and one spatial contiguity based matrix.

| Nearest neighbor | Inverse-distance | Contiguity | ||||

| Tests |

2 |

10 | 50 km | 200 km | ||

| cut-off | cut-off | |||||

| Spatial Error: | ||||||

| Moran’s I | 4.985 | 9.244 | 5.155 | 5.155 | 7.385 | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | ||

| LM | 21.379 | 62.846 | 39.584 | 29.281 | 44.261 | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | ||

| Spatial lag: | ||||||

| LM | 25.306 | 39.813 | 44.176 | 9.776 | 33.167 | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | ||

At least two conclusions can be drawn from the diagnostic tests. First, spatial dependence is present. All LM-tests are significant which indicates the presence of spatial dependence. Second, the diagnostic tests are in favor of the spatial error model as the LM-test concerning the spatial error model has a higher value compared to the value concerning the spatial lag model.

We continue our analysis to estimate a spatial Durbin model with all the different spatial weight matrices. We do that in order to test if the more general spatial Durbin model is preferred compared to the spatial error model and the spatial lag model. The test is carried out with a LR-test. The test statistics (33.24 and 46.25) are all higher than the critical value (18.31), which indicates that the hypothesis can be rejected. That is to say, the spatial Durbin model describes the data best2 . The results from the spatial Durbin model are presented in Table 5. The spatial weight matrix with the highest log likelihood is the contiguity matrix (see Table 6), and consequently, only the results from this specification are presented in Table 5 below. We have also estimated two diagnostic statistics concerning spatial autocorrelation in the residuals from the spatial Durbin model, namely LM-test and Moran’s I. The Moran’s I and LM-test is based on Anselin (2005) definition. Both of them show no indication of spatial dependency in the residuals.

|

Coefficients | Direct | Indirect | Total

| |||||

| effect

| ||||||||

| High house prices | 0. | 0839 | 0. | 0885 | 0. | 0814 | 0. | 1699 |

| (4. | 25) | (4. | 40) | (1. | 33) | (2. | 55) | |

| Change in house prices | 0. | 1456 | 0. | 1591 | 0. | 2305 | 0. | 3896 |

| (5. | 30) | (5. | 77) | (2. | 84) | (4. | 59) | |

| Human capital | 0. | 2487 | 0. | 2242 | -0. | 4373 | -0. | 2131 |

| (6. | 40) | (5. | 92) | (-3. | 63) | (-1. | 66) | |

| Establishments | -0. | 1683 | -0. | 2882 | -0. | 4229 | -0. | 7111 |

| (-2. | 39) | (-3. | 98) | (-1. | 70) | (-2. | 68) | |

| Self-employed | 0. | 2111 | 0. | 1916 | -0. | 3315 | -0. | 1399 |

| (3. | 54) | (3. | 12) | (-1. | 51) | (-0. | 58) | |

| Employment | 0. | 0216 | 0. | 0248 | 0. | 0577 | 0. | 0825 |

| (2. | 02) | (2. | 32) | (1. | 67) | (2. | 22) | |

| Income | 0. | 2346 | 0. | 3191 | 1. | 6344 | 1. | 9535 |

| (1. | 55) | (2. | 09) | (3. | 44) | (3. | 76) | |

| Unemployment | 0. | 0708 | 0. | 0597 | 0. | 1805 | 0. | 2402 |

| (2. | 37) | (1. | 76) | (2. | 21) | (2. | 93) | |

| In-migration | 0. | 0226 | 0. | 0143 | -0. | 031 | -0. | 0164 |

| (1. | 61) | (1. | 00) | (-0. | 84) | (-0. | 42) | |

| Stockholm | 0. | 1891 | 0. | 1842 | -0. | 0775 | 0. | 1068 |

| (3. | 91) | (3. | 87) | (-1. | 09) | (2. | 02) | |

| Rho | 0. | 422 | ||||||

| (5. | 52) | |||||||

| Constant | -7. | 7635 | ||||||

| (-4. | 52) | |||||||

| Log-likelihood | 405. | 449 | ||||||

| R2-adjusted | 0. | 8484 | ||||||

| LR-test statistics (SDM vs SEM) | 33. | 24 | ||||||

| LR-test statistics (SDM vs SAR) | 46. | 25 | ||||||

| LM test for spatial autocorrelation |

0.8898 | |||||||

| (Prob >z) | ||||||||

| Moran’s I (Prob >z) | 0. | 7492 | ||||||

By interpreting the coefficients we have the following results. If the proportion of the population with a university degree increases, the number of startups increases. That is, human capital is important as, for example, Armington, Acs (2002) and Lee et al. (2004) have shown. The same is true for an increase in the variables number of employees, income level, as well as unemployment rate. Our results are consistent with the findings of Armington, Acs (2002) and, more recently, Adelino et al. (2015) and Binet, Facchini (2015). The spillover effect (indirect effect) concerning human capital is negative indicating that lower human capital in neighboring municipalities is associated with fewer startups. However, the indirect effect concerning income and unemployment is positive, indicating spillover effect.

However, if the ratio between employment and establishment increases (the proxy for business set up), then the number of startups decreases. That is, regions with many SMEs are more likely to foster new startups. Our results concerning the Swedish market can confirm the results of Audretsch, Fritsch (1994) and those of Armington, Acs (2002), among others.

We can also observe that the number of self-employed persons in a labor market in 2007 leads to an increase in the number of startups per capita in the next seven years. Hence, the entrepreneurial climate seems to have an effect. The Melting Pot Index indicated that diversity is not significant in all models. Our results support the findings of Lee et al. (2004).

We can also notice a Stockholm effect. Being the capital, the Stockholm labor market fosters more startups per capita than the rest of Sweden. However, this effect alone cannot explain our findings. In fact, even if we exclude Stockholm, we can observe more or less the same results.

Housing market conditions represent the key determinant here. Two variables are used to measure housing prices. The first variable measures house price levels. It is a binary variable indicating whether the specific labor market has a price level that is above the national average house price level. The second variable measures house price growth. Both coefficients concerning housing market conditions are statistically significant and positive, indicating that a positive relationship exists between new firm formation and both house price appreciation and house price level, respectively. Our finding supports the results of Adelino et al. (2015) and of Balasubramanyan, Coulson (2013).

Hence, the change in startups per capita for the period 2007-2014 can be explained by determinants that measure either the situation in 2007 or the change between 2001 and 2007. We argue that this is a causal relationship and not merely a correlation. If the change in house prices increases by 1%, the expected change in startups is around 0.15%. We also observe that the number of startups per capita is higher if the house prices are above average in 2007, indicating that both the level and the change in house prices are of importance. If we consider the direct impacts, we can observe that these are close to the spatial Durbin model coefficients, that is, the results indicate that the feedback effects are very small and of no economic significance. Spatial spillover measured by the indirect effect is positive and statistically significant. One interpretation could be that this positive spillover effect reflects how changes in house prices in all regions would impact startups in their own region. The spillover effect may be a result from expectations of future house prices. The indirect effect concerning the variable high house prices is, however, not statistically significant, indicating no regional spillover.

In order to test the robustness of our estimated coefficients concerning high house prices and the change in house prices we have also estimated the spatial Durbin model using different spatial weight matrices. The results are presented in Table 6. As observed, the difference in estimated parameters is very small, that is our results are robust when it comes to choice of spatial weight matrix. For example, the coefficient concerning the variable high house prices ranges from 0.0817 to 0.1268 and the coefficient concerning change in house price ranges from 0.1465 to 0.2015. Most of the estimates are of the same magnitude. The exception is the spatial weight matrix based on inverse distance with a cut-offs of 200 kilometers.

| Spatial weight | Change in | High house | Log-likeli- |

| matrix | house price | price | hood |

| Nearest neighbor 2 | 0.1556 | 0.0990 | 386.497 |

| Nearest neighbor 10 | 0.1560 | 0.0817 | 399.016 |

| Inverse distance 50 | 0.1465 | 0.0923 | 398.463 |

| Inverse distance 200 | 0.2015 | 0.1268 | 390.913 |

| Continuity | 0.1456 | 0.0839 | 405.449 |

6 Conclusion and discussion

A number of interesting issues are highlighted in Section 5. For instance, most entrepreneurship theorists would agree that at the margin, there are nascent or potential entrepreneurs who lack access to finance. There also exist entrepreneurs at the margin who would remain self-employed longer if they had access to finance. However, assuming that people who suddenly receive money would generally use some or all of this money to start businesses would be an oversimplified view of the world. If potential entrepreneurs do not perceive an opportunity, or if they do not possess the unique capabilities necessary for exploiting a perceived opportunity, giving them money in itself is not enough (cf. Shane 2000).

In the present study, we have provided evidence that higher house prices – at an aggregate level – lead to an increase in business starts. A major contribution of our analysis lies in our modeling approach. We control for both endogeneity and spatial dependence of the entire population of Swedish municipalities. First, by separating observations in time, where the observation of house prices is in period n and the observation of entrepreneurship is in period n+1, we control for endogeneity and posit a causal relationship where higher house prices lead to an increase in entrepreneurial activity. Second, by employing a spatial Durbin model, we control for spatial dependence. We contribute to current theory by providing evidence in support of studies where house prices impact entrepreneurship. For policymakers, these results underline the paramount importance of the public sector’s capacity for urban planning and the need for efficient processes in the institutional framework regulating the housing sector.

In the future, we intend to conduct a more specific analysis of how increases in house prices affect start-up frequencies in different sectors and regions. Today, the most common type of start-up in Sweden is a service firm with other firms as customers, but we expect to see regional differences in terms of the types of firms that are started.

One potential limitation of our paper is that it is based on an analysis of a single national case, in our case Sweden. Sweden has a bank-oriented economy (along with other countries such as Japan and Germany), whereas the United States and the United Kingdom are examples of market-oriented economies (cf. Mayer 1988). It is difficult to ascertain to what extent and in what way this orientation affects individual transactions and relations, and while there surely exist different traditions in different countries in terms of entrepreneurial activity, one could also make the opposite argument that some aspects of economic activity are increasingly global in nature and not very different between industrialized nations today. However, the difference in orientation has historically pervaded all economic activity. Therefore, future research in this field should endeavor to compare results between bank- and market-oriented economies.

References

Abor J, Biekpe N (2009) How do we explain the capital structure of smes in sub-Saharan Africa?: Evidence from Ghana. Journal of Economic Studies 36: 83–97. CrossRef.

Acs ZJ, Audretsch DB, Feldman MP (1994) R&D spillovers and recipient firm size. Review of Economics and Statistics 76: 336–340

Adelino M, Schoar A, Severino F (2015) House prices, collateral, and self-employment. Journal of Financial Economics 117: 288–306. CrossRef.

Agostini L, Caviggioli F, Filippini R, Nosella A (2015) Does patenting influence SME sales performance? A quantity and quality analysis of patents in Northern Italy. European Journal of Innovation Management 18: 238–257. CrossRef.

Alon I, Rottig D (2013) Entrepreneurship in emerging markets: New insights and directions for future research. Thunderbird International Business Review 55: 487–492. CrossRef.

Andersson M, Klepper S (2013) Characteristics and performance of new firms and spinoffs in sweden. Industrial and Corporate Change 22: 245–280. CrossRef.

Andersson R, Mandell S, Wilhelmsson M (2014) Så skapas attraktiva städer. Reforminstitutet, isbn 978-91-980600-8-9

Anselin L (1988) Spatial Econometrics: Methods and Models. Kluwer, Dordrecht. CrossRef.

Anselin L (2005) Exploring spatial data with geoDaTM: A Workbook. Center for spatially integrated social science. revised version, march 6, 2005

Anselin L, Bera A, Florax R, Yoon MJ (1996) Simple diagnostic tests for spatial dependence. Regional Science and Urban Economics 26: 77–104. CrossRef.

Arena for Growth (2015) The new geography of sweden. Arena for growth, Stockholm

Armington C, Acs ZJ (2002) The determinants of regional variation in new firm formation. Regional Studies 36: 33–45. CrossRef.

Atherton A (2012) Cases of start-up financing: An analysis of new venture capitalisation structures and patterns. International Journal of Entrepreneurial Behavior & Research 18: 28–47

Audretsch D, Fritsch M (1994) The geography of firm births in Germany. Regional Studies 28: 359–365. CrossRef.

Balasubramanyan L, Coulson E (2013) Do house prices impact business starts? Journal of Housing Economics 22: 36–44. CrossRef.

Bateman M (2000) Neo-liberalism, SME development and the role of business support centres in the transition economies of Central and Eastern Europe. Small Business Economics 14: 275–298

Berger AN, Udell GF (1998) The economics of small business finance: The roles of private equity and debt markets in the financial growth cycle. Journal of Banking & Finance 22: 613–673

Berggren B, Olofsson C, Silver L (2000) Control aversion and the search for external financing in swedish SMEs. Small Business Economics 15: 233–242

Bernanke BS, Gertler M, Gilchrist S (1999) The financial accelerator in a quantitative business cycle framework. In: Taylor J, Woodford M (eds), Handbook of macroeconomics: vol. 1. North Holland, Amsterdam. CrossRef.

Binet ME, Facchini F (2015) The factors determining firm start-ups in French regions and the heterogeneity of regional labor markets. Annals of Regional Science 54: 251–268. CrossRef.

Birch DGW (1979) The job generation process. MIT Program on Neighborhood and Regional Change 302

Black J, de Meza D, Jeffreys D (1996) House prices, the supply of collateral and the enterprise economy. Economic Journal 106: 60–75. CrossRef.

Bracke P, Hilber C, Silva O (2013) Homeownership and entrepreneurship: The role of commitment and mortgage debt. Institute for the Study of Labor (IZA) discussion paper no. 7417, IZA, Bonn

Cassar G (2004) The financing of business start-ups. Journal of Business Venturing 19: 261–283. CrossRef.

Chaney T, Sraer D, Thesmar D (2012) The collateral channel: How real estate shocks affect corporate investment. American Economic Review 102: 2381–2409. CrossRef.

Chasco C (2013) GeoDaSpace: A resource for teaching spatial regression models. React@, Monogràfico 4: 119–144

Davidsson P, Lindmark L, Olofsson C (1995) Small firms, business dynamics and differential development of economic well-being. Small Business Economics 7: 301–315. CrossRef.

Davidsson P, Steffens P, Fitzsimmons J (2009) Growing profitable or growing from profits: Putting the horse in front of the cart? Journal of Business Venturing 24: 388–406. CrossRef.

De Clercq D, Lim D, CH O (2013) Individual-level resources and new business activity: The contingent role of institutional context. Entrepreneurship Theory and Practice 37: 303–330. CrossRef.

Degryse H, de Goeij P, Kappert P (2012) The impact of firm and industry characteristics on small firms’ capital structure. Small Business Economics 38: 431–447. CrossRef.

Doh S, Kim B (2014) Government support for SME innovations in the regional industries: The case of government financial support program in South Korea. Research Policy 43: 1557–1569. CrossRef.

Donaldson G (1984) Managing corporate wealth: The operation of a comprehensive financial goals system. Praeger, New York

Elhorst JP (2010) Applied spatial econometrics. Spatial Economic Analysis 5: 9–28. CrossRef.

GEM (2012) Entrepreneurship in Sweden: National Report. Entrepreneurship Forum, Stockholm

Gordon IR, McCann P (2005) Innovation, agglomeration, and regional development. Journal of Economic Geography 5: 523–543. CrossRef.

Greenspan A, Kennedy J (2008) Sources and uses of equity extracted from homes. Oxford Review of Economic Policy 24: 120–144. CrossRef.

Gregory BT, Rutherford MW, Oswald S, Gardiner L (2005) An empirical investigation of the growth cycle theory of small firm financing. Journal of Small Business Management 43: 382–392. CrossRef.

Halilem N, Bertrand C, Cloutier JS, Landry R, Amara N (2012) The knowledge value chain as an SME innovation policy instrument framework: An analytical exploration of SMEs public innovation support in OECD countries. International Journal of Technology Management 58: 236–260. CrossRef.

Halleck Vega S, Elhorst J (2013) On spatial econometric models, spillover effects, and W. Working paper, Faculty of Economics and Business, University of Groningen

Harding R, Cowling M (2006) Assessing the scale of the equity gap. Journal of Small Business and Enterprise Development 13: 115–132. CrossRef.

Howorth CA (2001) Small firms’ demand for finance: A research note. International Small Business Journal 19: 78–86. CrossRef.

Hurst E, Lusardi A (2004) Liquidity constraints, household wealth, and entrepreneurship. Journal of Political Economy 112: 319–347. CrossRef.

Iacoviello M (2005) House prices, borrowing constraints, and monetary policy in the business cycle. American Economic Review 95: 739–764. CrossRef.

Jensen MC, Meckling WH (1976) Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3: 305–360. CrossRef.

Jin Y, Leung CKY, Zeng Z (2012) Real estate, the external finance premium and business investment: A quantitative dynamic general equilibrium analysis. Real Estate Economics 40: 167–195. CrossRef.

Johannisson B (1984) A cultural perspective on small business – local business climate. International Small Business Journal 2: 32–43

Johnsen GJ, McMahon RGP (2005) Owner-manager gender, financial performance and business growth amongst SMEs from Australia’s business longitudinal survey. International Small Business Journal 23: 115–142. CrossRef.

Keeble D (1997) Small firms, innovation and regional development in Britain in the 1990s. Regional Studies 31: 281–293. CrossRef.

Lee SY, Florida R, Acs Z (2004) Creativity and entrepreneurship: A regional analysis of new firm formation. Regional Studies 38: 879–891. CrossRef.

LeSage J, Pace RK (2009) Introduction to Spatial Econometrics. Chapman & Hall/CRC, Boca Raton. CrossRef.

LeSage J, Pace RK (2014) The biggest myth in spatial econometrics. Econometrics 2: 217–249. CrossRef.

Love JH, Roper S (2015) SME innovation, exporting and growth: A review of existing evidence. International Small Business Journal 33: 28–48. CrossRef.

Mac an Bhaird C, Lucey B (2011) An empirical investigation of the financial growth lifecycle. Journal of Small Business and Enterprise Development 18: 715–731. CrossRef.

MacMillan HP (1931) Committee on finance and industry: report. Cmnd 4811, His Majesty’s Stationery Office (hmso), London

Manove M, Padilla J, Pagano M (2001) Collateral versus project screening: A model of lazy banks. RAND Journal of Economics 32: 726–744. CrossRef.

Mayer C (1988) New issues in corporate finance. European Economic Review 32: 1167–1183. CrossRef.

Mendiola L, Gonzàles P, Cebollada A (2015) The relationship between urban development and the environmental impact mobility: A local case study. Land Use Policy 43: 119–128. CrossRef.

Myers SC (1984) The capital structure puzzle. Journal of Finance 39: 574–592. CrossRef.

Newman A, Gunessee S, Hilton B (2012) The applicability of financial theories of capital structure to the Chinese cultural context: A study of privately owned SMEs. International Small Business Journal 30: 65–83. CrossRef.

Paul S, Whittam G, Wyper J (2007) The pecking order hypothesis: Does it apply to start-up firms? Journal of Small Business and Enterprise Development 14: 8–21. CrossRef.

Perren L, Jennings PL (2005) Government discourses on entrepreneurship: Issues of legitimization, subjugation, and power. Entrepreneurship Theory and Practice 29: 173–184. CrossRef.

Psillaki M, Daskalakis N (2009) Are the determinants of capital structure country or firm specific? Small Business Economics 33: 319–333. CrossRef.

Ramlall I (2014) Is there a pecking order in the demand for financial services in Mauritius? Journal of African Business 15: 49–63. CrossRef.

Revest V, Sapio A (2012) Financing technology-based small firms in Europe: What do we know? Small Business Economics 39: 179–205. CrossRef.

Robb AM, Robinson DT (2014) The capital structure decisions of new firms. Review of Financial Studies 27: 153–179. CrossRef.

Robson MT (1996) Housing wealth, business creation and dissolution in the UK regions. Small Business Economics 8: 39–48. CrossRef.

Ross SA (1973) The economic theory of agency: The principal’s problem. American Economic Review 63: 134–139

Santarelli E, Tran HT (2012) Growth of incumbent firms and entrepreneurship in Vietnam. Growth and Change 43: 638–666. CrossRef.

Schäfer D, Talavera O, Weir C (2011) Entrepreneurship, windfall gains and financial constraints: Evidence from Germany. Economic Modelling 28: 2174–2180. CrossRef.

Schmalz MC, Sraer DA, Thesmar D (2013) Housing collateral and entrepreneurship. Working paper 19680, National Bureau of Economic Research (NBER), Cambridge, MA. CrossRef.

Shane SA (2000) A general theory of entrepreneurship: The individual-opportunity nexus. Edward Elgar, Cheltenham

Stakhovych S, Bijmolt THA (2009) Specification of spatial models: A simulation study on weights matrices. Papers in Regional Science 88: 389–408. CrossRef.

Statistics Sweden (2015) Business activities. http://www.scb.se/en_/Finding-statistics/Statistics-by-subject-area/Business-activities/

Stiglitz JE, Weiss A (1981) Credit rationing in markets with imperfect information. American Economic Review 71: 393–410

Storey DJ, Greene FJ (2013) Small business and entrepreneurship. Pearson, Harlow

Vanacker TR, Manigart S (2010) Pecking order and debt capacity considerations for high-growth companies seeking financing. Small Business Economics 35: 53–69. CrossRef.

Weston JF, Brigham EF (1981) Managerial finance (7th edition ed.). Dryden Press, Hinsdale, IL

Wilhelmsson M (2002) Spatial models in real estate economics. Housing, Theory and Society 19: 92–101. CrossRef.