Volume

3, Number 1, 2016, 43-67 journal homepage:

region.ersa.org

Volume

3, Number 1, 2016, 43-67 journal homepage:

region.ersa.orgDOI: 10.18335/region.v3i1.121

Subjective Wellbeing Impacts of National and Subnational Fiscal Policies*

1 Motu Economic and Public Policy Research, and Victoria University of Wellington, Wellington, New Zealand (email: arthur.grimes@motu.org.nz)2 Motu Economic and Public Policy Research, Wellington, New Zealand (email: judd.ormsby@motu.org.nz)

3 Motu Economic and Public Policy Research, Wellington, New Zealand (email: anna_robinson@hotmail.com)

4 University of Auckland, Auckland, New Zealand (email: siuyuat@gmail.com) Received: 14 January 2016/Accepted: 30 March 2016

*This research was funded by Marsden Fund grant MEP1201 from the Royal Society of New Zealand. We are grateful for this assistance. We thank seminar participants at the New Zealand Association of Economists conference (July 2015) and the European Regional Science Association conference (September 2015) for their helpful comments. We also thank three anonymous referees as well as Phillip Morrison and Norman Gemmell for their comments on an earlier version. The usual disclaimer applies.

Abstract. We study the association between fiscal policy and subjective wellbeing using fiscal data on 35 countries and 130 country-years, combined with over 170,000 people’s subjective wellbeing scores. While past research has found that ‘distortionary taxes’ (e.g. income taxes) are associated with slow growth relative to ‘non-distortionary’ taxes (GST/VAT), we find that distortionary taxes are associated with higher levels of subjective wellbeing than non-distortionary taxes. This relationship holds when we control for macro-economic variables and country fixed effects. If this relationship is causal, it would offer an explanation as to why governments pursue these policies even when they harm economic growth. We find that richer people’s subjective wellbeing is harmed less by indirect taxes than for people with lower incomes, while “unproductive expenditure” is associated with higher wellbeing for the middle class relative to others, possibly reflecting middle class capture. We see little evidence for differential effects of fiscal policy on people living in different sized settlements. Devolving a portion of expenditure to subnational government is associated with higher subjective wellbeing but devolving tax collection to subnational government is associated with monotonically lower subjective wellbeing.

JEL classification: D60, E62, H50, H70, O57

Key words: Subjective wellbeing, Fiscal policy, Decentralized government

1 Introduction

Beginning with Barro (1990), there have been a number of endogenous growth models that attempt to understand the impacts of fiscal policy on both growth and wellbeing. Many researchers have attempted to empirically test the model’s predictions for economic growth, but economic growth is only a means to an end – the end being greater wellbeing. Despite this, far less attention has gone to testing the endogenous growth model’s implications for wellbeing. We help to fill this gap by connecting the fiscal policy and growth literature to the subjective wellbeing (SWB) literature.

To the best of our knowledge this study is the first in the SWB literature to explicitly consider the government budget constraint, the first to consider SWB within the context of endogenous growth theory, one of few (including within the growth literature) to use the IMF’s higher quality general (rather than central) government fiscal data, and the first to examine regional and subnational dimensions of the relationship of fiscal policies with subjective wellbeing.

While previous literature has argued that ‘non-distortionary’ indirect (sales) taxes are good for economic growth relative to ‘distortionary’ taxes, we find that distortionary taxes are associated with relatively higher levels of subjective wellbeing than are non-distortionary taxes. This result is robust to several different specifications. In addition, we find some indication that indirect taxes hurt the poor more than the rich, and we find the opposite relationship for distortionary taxation. As the model of Alesina, Rodrik (1994) predicts, we find evidence that productive expenditures benefit the poor relatively more than the rich. This result is not driven by people’s political ideology, supporting the idea that fiscal policies affect wellbeing through effects on the real economy. “Unproductive expenditure” appears to benefit the middle class by more than it benefits the rich or poor, consistent with middle class capture as predicted by the median voter model.

We also study the impacts on subjective wellbeing of devolving government expenditure and taxation to subnational government. We find devolution of taxation is associated with lower subjective wellbeing, while partial devolution of expenditure is associated with higher subjective wellbeing. This is consistent with subnational authorities having better information on their constituents’ wants and thus better ability to target resources. Taxation may be more simply administered by central government and the advantages to being better informed by constituents may be outweighed by economies of scale.

We find little variation when we interact fiscal policies with settlement size variables. Thus rural residents apparently have similar subjective wellbeing reactions to alternative fiscal policies as their urban counterparts.

We control for many unobservable and observable factors that affect fiscal policy and subjective wellbeing; importantly we control for country fixed effects, survey wave (i.e. time) fixed effects, personal characteristics, and country-specific, time-varying macroeconomic conditions. Our results can be interpreted causally if, aside from the variables that we already control for (including our macroeconomic controls), there are no other country-specific, time-varying factors that affect both fiscal policy and subjective wellbeing or any reverse causality from subjective wellbeing to fiscal policy. This is known as the parallel trends assumption1 . We find it plausible that trends are parallel, especially after controlling for macro-economic variables, since we have not identified other country-specific, time-varying omitted factors that would bias our results. There is also no obvious reason why there would be reverse causality. However fiscal policy is chosen by countries (rather than randomly allocated) in part to reflect their changing circumstances, so we cannot completely eliminate the possibility that these decisions depend on some unobserved time-varying, country-specific variables that also affect subjective wellbeing2 . We leave it to future research to analyze further the causal pathways that may underpin the relationships that we estimate.

Section 2 of the paper reviews the relevant theory. We discuss our data in Section 3, describe our methodology in Section 4, present our results in Section 5, and conclude in Section 6.

2 Theoretical framework

2.1 The Barro framework

Barro (1990) examined the role of fiscal policy within an endogenous growth framework – extending the previous work of Lucas (1988), Rebelo (1991), Romer (1986, 1988). Barro sets up a simple infinitely-lived representative agent model with lifetime utility, U, given by Equation (1).

| (1) |

where ρ > 0 is the rate of time preference and ut is instantaneous utility. Crucially instantaneous utility, ut, depends on both private consumption, ct, and government consumption services ht. Because ht enters the utility function directly and not the production function it has been termed as an unproductive expenditure in the successive literature (e.g. Kneller et al. 1999, Bleaney et al. 2001, Angelopoulos et al. 2007). In addition to providing consumption services, the government also funds productive expenditures, gt, that enter the production function alongside private capital (kt):

| (2) |

where yt is aggregate output. As is standard in endogenous growth theory, Φ exhibits constant

(or increasing) returns to scale. The full detail of the model is spelled out in Barro (1990). One

of Barro’s key results is that an increase in the share of output devoted to unproductive

expenditures (ht∕yt in the notation above) reduces growth of output, capital and

consumption, but potentially increases lifetime utility. As Barro and Sala-i-Martin

put it in a later paper: “An increase in ![[ht]

yt](121-new7x.png) can be consistent with an increase in

utility that accompanies a decrease in the growth rate” (Barro, Sala-i Martin 1992,

651)3 .

The growth slowdown occurs because the increase in income taxes lowers the private marginal

product of capital, discouraging private investment; however, if the additional tax revenue is

used to provide public services valued by households (ht), overall utility may be

raised.

can be consistent with an increase in

utility that accompanies a decrease in the growth rate” (Barro, Sala-i Martin 1992,

651)3 .

The growth slowdown occurs because the increase in income taxes lowers the private marginal

product of capital, discouraging private investment; however, if the additional tax revenue is

used to provide public services valued by households (ht), overall utility may be

raised.

The Barro model only includes income taxes and lump sum taxes. Labor supply is treated as perfectly inelastic and so consumption taxes are equivalent to a lump-sum tax. This has led to the potentially confusing convention of referring to consumption, sales, and value-added taxes (i.e. indirect taxes) as non-distortionary taxation in the subsequent empirical literature – again see, for example, Bleaney et al. (2001), Kneller et al. (1999), Angelopoulos et al. (2007). With endogenous labor supply, such consumption taxes are distortionary. With this qualification noted, we will continue with the terminology of previous authors so as to make our analysis comparable with theirs.

In the Barro model, with a representative agent, the socially optimal outcome cannot be obtained by income taxation as it distorts private incentives to save. Meanwhile lump-sum taxes produce a higher level of growth than income taxes but they too can fail to generate the socially optimal output level, as the optimum requires getting the government size just right4 . With heterogeneous agents who value unproductive expenditures differently, the simple results from this model with regard to fiscal categories may no longer hold.

There have been many extensions to the basic Barro model. Misch et al. (2013) and also Baier, Glomm (2001) show that optimal fiscal policy depends on the degree of complementarity between g and k: a high degree of complementarity results in a larger optimum government size and an optimal growth rate that is lower than the growth-maximizing one5 . The importance of transitional dynamics is shown both by Baier, Glomm (2001) and Futagami et al. (1993). Turnovsky (2000) adds endogenous labor supply, demonstrating that an equilibrium growth path may not even exist. With endogenous labor-leisure trade-offs, consumption taxes become distortionary unlike in Barro (1990). This additional literature demonstrates that welfare maximizing fiscal policy is complex: the optimal policy setting depends on the exact model and is therefore an empirical question.

One last model, especially relevant to our work, is that of Alesina, Rodrik (1994). Alesina and Rodrik take the Barro framework and introduce variation in people’s ownership of capital. In this model, the welfare of a pure capitalist – someone whose income is entirely from capital – is maximized when the growth rate is maximized, but all others prefer higher taxation and lower growth (and the lower their share of capital relative to labor income, the higher taxes they desire). The higher taxes are useful to laborers not through direct cash transfers, but because government-provided capital increases labor productivity. We test – and find some support for – the hypothesis that productive expenditure disproportionally benefits the poor6 .

2.2 Theory meets empirics

Nijkamp, Poot (2004) conducted a meta-analysis of 93 empirical journal articles on the effects of fiscal policies on growth, finding mixed results for these effects. A key problem with many of the early papers that they reviewed is that the papers rarely gave due consideration to the government’s budget constraint. For example, papers tested for the effects of taxation without controlling for how revenues are spent, or tested for the effects of government spending without controlling for how the revenues are raised. One exception is Bleaney et al. (2001), whose methodology we adapt for subjective wellbeing. We outline their approach in our methodology section.

2.3 SWB and fiscal policy literature

There is only a small and recent literature on the effects of fiscal policies on subjective wellbeing. The results are mixed. For example, several papers look at the relationship between the size of government consumption and subjective wellbeing. Results include finding a negative relationship (Bjørnskov et al. 2007, Oishi et al. 2011), finding no relationship (Ram 2009), finding a positive relationship (Flavin et al. 2011, 2014), and finding an inverse U pattern (Hessami 2010). Other papers have looked at taxation with Flavin et al. (2011, 2014) finding higher taxation associated with higher SWB. Oishi et al. (2011) find more progressive tax systems are correlated with higher SWB. Veenhoven (2000) examines social security generosity and finds no relationship with SWB.

Most of these papers are cross sectional. Only Flavin et al. (2011, 2014) and Veenhoven (2000) estimate country fixed effects, despite the obvious importance of country effects for both SWB (e.g. through culture) and fiscal policy (again possibly through culture, or through circumstances like natural resource endowments)7 . None of these papers takes into account the structure of taxation or how government consumption is financed, and none of these papers uses the high quality IMF general government data.

2.3.1 SWB validation

SWB has become increasingly recognized as an important area of study as research has validated it as an informative measure of wellbeing. SWB is highly correlated in test-retest comparisons of the same individual a short time apart (e.g. see Diener et al. 2013). While some studies have shown that SWB can be influenced by seemingly arbitrary factors (e.g. Schwarz 1987), on average these vicissitudes will wash out in large samples such as ours. Many studies show a good correlation between SWB and other subjective and objective measures of wellbeing. For example, within a given country those who are richer are more satisfied with their lives, and across countries, developing countries are less satisfied than developed ones. Stevenson, Wolfers (2008) show that these cross-sectional relationships remain robust when considered in a time series context unlike the earlier findings of Easterlin (1974). Stevenson and Wolfers emphasize the log-linear rather than linear nature of the relationship between GDP per capita and SWB. They also emphasize that the positive point estimate for the relationship is robust even if its statistical significance is less so in some subsamples8 . Helliwell, Huang (2008) show that life satisfaction is closely correlated with many of the World Bank’s measures of good government. Di Tella et al. (2003) find that recessions lower SWB. Finally studies in other fields have found evidence that SWB correlates with other measures of people’s welfare9 .

Several studies have found differences in rural versus urban SWB (Easterlin et al. 2011, Morrison 2011, Berry, Okulicz-Kozaryn 2011, 2009, Veenhoven 1994)10 . For these reasons we include controls for settlement size and test whether relationships differ across large versus small settlements.

3 Data

3.1 Fiscal Variables

The majority of our fiscal data is sourced from the IMF Government Finance Statistics database (IMF 2014), supplemented with OECD data where IMF data is missing (OECD 2014). Unlike almost all previous studies (in both the SWB and growth literature), we make use of general government as well as central government data: the former provides us with a more complete picture of a nation’s fiscal policy settings, while the latter has better coverage. The use of both datasets together allows us to explore the SWB effects of decentralization of fiscal policy.

Following the Barro model, we split each of expenditure and taxation into two main categories: distortionary and non-distortionary taxation, and productive and unproductive expenditures. We also include two residual categories, “other revenue”, OR, and “other expenditure”, OE, plus the budget surplus (BS). Our taxonomy is the same as in much of the empirical growth literature; specifically we use the definitions of Bleaney et al. (2001) to make our results for the effects of fiscal policy on SWB directly comparable with their results for the effects on growth. These category definitions are described in detail in Table A.1. Broadly speaking, non-distortionary taxation, NDT, is defined as indirect taxes on goods and services (i.e. GST/VAT), while distortionary taxation, DT, is taxation on income, social security contributions, and property taxes. Productive expenditures, PE, include education, health, housing, transport, defense and general public services. Unproductive expenditures, UE, include social security and welfare, recreation and economic services. Each of these variables is expressed as a percentage of the country’s GDP11 . Summary statistics of these, and other country-level variables, can be found in Table A.2. More details about our data cleaning process can be found in the Appendix, as well as in our Stata code.

3.2 Subjective wellbeing and personal controls

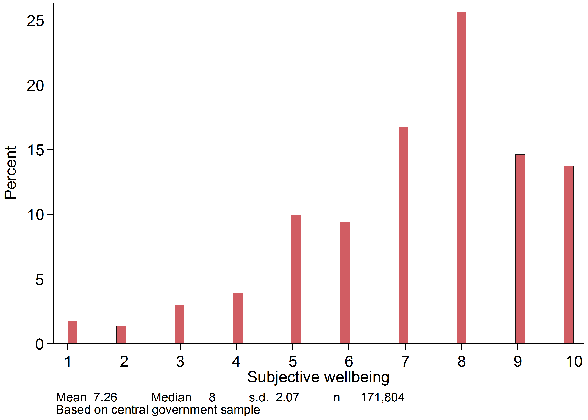

We use data on subjective wellbeing (SWB) from the World Values Survey (WVSA 2014) and the European Values Survey (EVS 2011). Subjective wellbeing is asked (in the local language) as:

|

All things considered, how satisfied are you with your life as a whole these days? Please use this card to help with your answer. ‘Dissatisfied’ 1 2 3 4 5 6 7 8 9 10 ‘Satisfied’. |

Both WVS and EVS include information on people’s age, gender, education, settlement size, and political orientation. Table A.3 provides summary statistics for key variables. We include age in six categories14 , education in eight categories15 , and settlement size in four categories16 . Political orientation and income are measured on a 10 point scale, entered in our regressions as categorical variables17 . For each of these variables we include two extra categories for missing information: missing because the question was not asked in the survey, and missing for other reasons18 . Finally we include a dummy variable to distinguish between the WVS and the EVS.

Donnelly, Pop-Eleches (2012) criticize the WVS and EVS measures of income. They point out that the income distributions associated with these 10 categories are not usually interpretable as deciles, as some researchers have interpreted them, and that the method used to record income varies. In the vast majority of surveys (210 out of 245), respondents are asked to place themselves in one of 10 income brackets (e.g. $0-$1,000, $1,000–$5000 etc.), where the brackets available were pre-determined by WVS/EVS, though 58 of these countries are missing documentation on the exact brackets used (Donnelly, Pop-Eleches 2012, 3). These brackets often do not generate uniform decile distributions of income. In other cases, respondents are asked to subjectively place themselves on a ten point scale where 1 represents the first decile and 10 the highest. In such cases, most people respond with a middle number: for example 84% of Americans in the 2006 wave claim they are in one of the middle 5 deciles (deciles 3-7). Finally in some cases respondents are asked to write down their income, whereby WVS/EVS later recode it onto a ten point scale, in some cases to match pre-determined brackets, in other cases to perfectly split the data into ten equally populated deciles.

Because of these survey inconsistencies we interpret income purely as an ordinal variable within a given country year: i.e. if somebody is on a higher income step than someone else in the same country-year they likely earn more, but we do not know the cardinal relationships between categories.

3.3 Macroeconomic controls

In most specifications we include controls for real PPP-adjusted GDP per capita (current and lagged three years), unemployment, investment, and inflation. We calculate real GDP per capita as real PPP-adjusted GDP divided by population, with both figures coming from the Penn World Tables, version 8.1 (Feenstra et al. 2015) except in the case of 2012 data, where we use data from the World Bank (The World Bank 2015b)19 . Our primary source of data on unemployment is from the Annual Macro Economics Database (European Commission 2015). For countries where we do not have AMECO data we use the World Bank development indicators data, (The World Bank 2015c) spliced, where necessary, with UN unemployment data (The United Nations 2015)20 . We source inflation data for all but three countries from the World Bank development indicators21 . All investment data is from the World Bank development indicators (The World Bank 2015b,c)22 . Table A.4 lists the countries used in each of our regressions.

4 Methodology

Equation (3) illustrates our baseline equation. We estimate subjective wellbeing for individual i in country c at time t as a function of our fiscal variables, F, a vector of personal controls, X, a vector of macro controls, M, country fixed effects, λc, and survey wave (time) fixed effects, λw.

with the budget surplus BS omitted to avoid perfect multicollinearity. In other specifications we make some modifications to Equation (3), e.g. removing the macro controls, including an interaction of our fiscal variables with income and political affiliation, and including the proportion of each fiscal category which is spent subnationally.

Our analysis includes countries only if we observe them in more than one year. This allows us to estimate country fixed effects λc. Researchers have worried about whether the SWB question is understood the same way across different countries. Separately, different cultures may have different average levels of subjective wellbeing. In both cases, failure to control for these could bias our estimate of βF. Country fixed effects allow us to control for, among other things, constant cultural effects over time23 .

In addition to country fixed effects, we control for survey wave fixed effects, λw. The survey waves are: 1981-84, 1989-93, 1994-98, 1999-04, 2005-09, 2010-1224 . These are important as they allow us to control for any changes in survey practices across survey wave. For example the order of question and types of questions elsewhere in the survey can change, possibly affecting people’s responses. The wave fixed effects will also pick up global shocks to macro and other variables (for example global recessions such as the global financial crisis which may affect both SWB and our fiscal variables).

The government’s budget constraint requires that in each year all taxes be spent or saved, and that all expenditure be funded by taxation or borrowing. Formally:

| (4) |

As Bleaney et al. (2001) emphasize, it is vital to recognise the government’s budget constraint when analysing the effects of fiscal policy. Fiscal policy does not occur in a vacuum: expenditure must be financed, and taxes must be spent or saved. If one looks at a variable in isolation, say productive expenditure, then one cannot obtain a clear picture of its impact on wellbeing because its effect on wellbeing will depend on whether it is funded from reducing unproductive expenditures, increasing distortionary or non-distortionary taxes, or by borrowing the funds.

Because of the perfect collinearity described in Equation (4) one category must be omitted when we estimate Equation (3). The coefficients on each fiscal variable are then interpreted as the effect of increasing that variable by one unit financed by changing the omitted category. In our regressions we omit the budget surplus, so that for an increase in an expenditure variable the assumption is that the surplus is reduced, while for taxation variables the assumption is that the surplus is increased.

After estimating Equation (3) with the surplus omitted, it is trivial to compute the

associations relative to an alternative financing assumption. One simply adds or subtracts the

coefficients estimated in Equation (3); for example, to find the effect of increasing PE by one

percent of GDP funded by increasing DT one should add  and

and  . If the increase

in PE were instead funded by reducing UE, then one should subtract

. If the increase

in PE were instead funded by reducing UE, then one should subtract  from

from

.

.

The effects of fiscal policies could be nonlinear. For example, perhaps a small amount of non-distortionary taxation is beneficial for SWB, while too much is detrimental. One way of dealing with such nonlinearities would be to include polynomials into the specification. However, given the complication of the government’s budget constraint, marginal effects would then become difficult to interpret. Whether, say, more distortionary taxation funded from a reduction in non-distortionary taxation was beneficial for SWB would depend on the existing amount of both distortionary and non-distortionary taxation. In addition to the issues of interpretation, we are wary of overfitting the model, and picking up outliers, if we were to estimate such nonlinearities. The same problems present themselves for the fiscal policy and growth literature (discussed above) and we are not aware of papers that deal with both the government’s budget constraint and nonlinearities in fiscal policy. Given the difficulties in adequately dealing with these issues we leave analysis of the impacts of such nonlinearities for separate research.

All our equations are estimated using OLS with two-way fixed effects and a suite of personal and macroeconomic controls. As discussed above, fiscal policies are chosen, rather than being randomly assigned. One can think of isolated cases where a shock to most individuals’ wellbeing is correlated with shocks to one or more fiscal variables. For instance, even in the absence of any macroeconomic effects, a terrorist attack may lower SWB while raising defense expenditure. Intuitively, however, such examples appear to be isolated, especially once any conduits through macroeconomic conditions are controlled for. At a practical level randomization of fiscal policy is off the table, and suitable instruments for fiscal policy variables are hard to come by since most variables that are correlated with fiscal policy could also directly affect SWB. Even if one could find instruments that satisfy the exclusion restriction, they would need to be strong, and no strong instruments present themselves. While our study is at least as well identified as the fiscal policy and growth literature, we still speak of associations or relationships rather than causal connections because we cannot definitively rule out violations of parallel trends.

5 Results

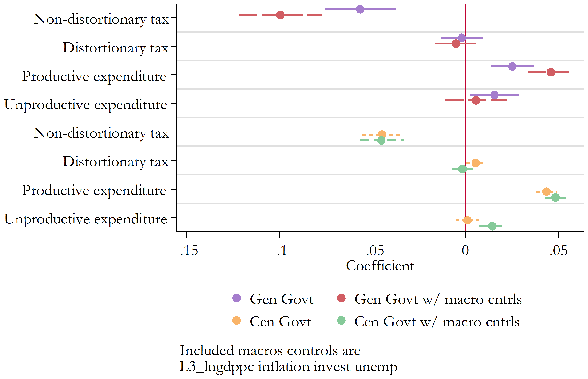

As emphasized in the previous section, when estimating the effects of fiscal categories on wellbeing (or growth), none of the fiscal coefficients can be interpreted in isolation. To aid comparisons of coefficients with each other, we plot the estimated coefficients graphically together with their 90% confidence intervals. Detailed regression tables for Figure 1 and Figure 5 can be found in the appendix25 .

5.1 Baseline Results

Figure 1 plots the coefficients from four different regressions. The top set of results (i.e. the first four listed fiscal categories) uses the general government data as our fiscal variables, F, whilst the bottom set of results use the central government data. A coefficient of zero implies that an increase in that variable has the same effect on SWB as the omitted category – the surplus. For each regression, we present results without macroeconomic controls (the upper of each pair) and with the inclusion of macroeconomic controls to show whether results are sensitive to their inclusion. All regressions contain the controls for personal characteristics.

In all four regressions, distortionary taxes are associated with higher subjective wellbeing than non-distortionary taxation, and productive expenditures are associated with higher subjective wellbeing than unproductive expenditures. Adding macro controls makes very little difference to the results: non-distortionary taxation appears to be worse for SWB when macro controls are added to the general government regression, but the effect is imprecisely estimated (as evidenced by the wide confidence intervals), and the point estimate hardly changes when macro controls are added to the central government regression.

The magnitude of the coefficients shows the SWB effect of a 1 percentage point-sized change in the fiscal variable (funded by changing the surplus) as a proportion of GDP. The differences between different tax and expenditure estimates are economically meaningful. For example, reducing distortionary taxation by 10 percent of GDP funded by a same sized rise in non-distortionary taxation is associated with an approximate 0.6 unit rise in SWB, about 25% of a standard deviation. This effect is larger than the (transitory) effect of getting married found in Clark et al. (2008), and it is enough to move a country’s subjective wellbeing rank from around 15th out of the 34 OECD countries to about 5th.

5.2 Differential effects of fiscal policy

We examine whether the impacts of fiscal policy on SWB vary according to income and political persuasion. Noting the similarity of results above using central and general government definitions, and given the larger sample size afforded by the central government dataset, we estimate these equations based on the central government data. All results in this section include all macro and personal controls.

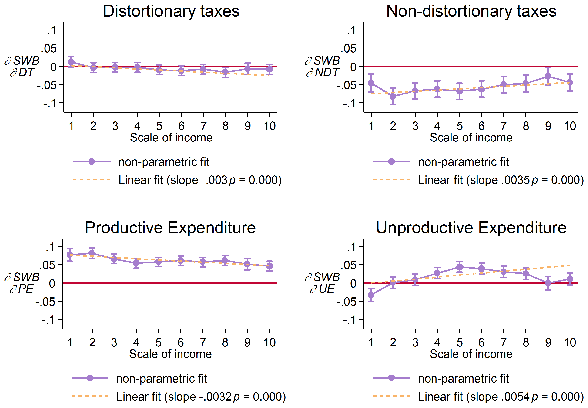

5.2.1 Income

With progressive income taxes, higher income earners pay a higher percentage of their income in income tax than low income earners, while under consumption taxes poorer people pay a higher percentage of their income than high income earners (assuming that poorer people save less). Given these differences in incidence, we explore whether people at different parts of the income spectrum have different SWB responses to the various fiscal categories.

We examine these effects in two ways. First, we treat income as a continuous variable and interact it linearly with each fiscal category. Second, we treat income as a categorical variable and interact each income category with each of the four main fiscal policies FM as in equation (5):26

| (5) |

This non-parametric approach does not impose any functional form assumption, but has the drawback of decreasing the precision of our estimates.

Figure 2 plots the marginal effects of our fiscal variables from both specifications across the ten income ranks27 . The dashed lines present the marginal effects of the linearly interacted variable, with the slope estimate and its associated p-value displayed beneath each graph. The solid line links the non-parametric estimates (with associated 90% confidence intervals). As expected, our results indicate that distortionary taxation has a more negative effect for higher income earners, and non-distortionary taxation has a more negative effect on lower income earners. Productive expenditure also appears to be favored by poorer individuals, consistent with Alesina, Rodrik (1994), where productive expenditure especially improves the welfare of unskilled laborers (see Section 2).

The results for unproductive expenditures, which mainly comprises social welfare spending, is found to have most benefit for the middle class and least benefit for poorer people. Indeed, the point estimate for the poorest people is negative. This result is consistent with middle class capture, as in median voter models28 . An alternative explanation is that this result could reflect the countercyclical nature of unproductive expenditures combined with an assumption that business cycles affect the poor the most and the middle class the least. To minimize this potential source of bias, our estimates include controls for unemployment, investment, inflation, current GDP and lagged GDP, so this alternative explanation would require that these variables do not sufficiently control for the business cycle.

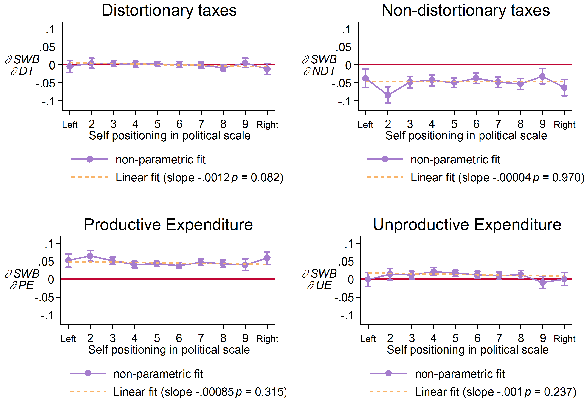

5.2.2 Political orientation

It is possible that fiscal policy affects utility directly through political preferences (ideologies) instead of through the fiscal policy’s influence on the real economy (h and c). We examine whether this may be the case. If such a phenomenon were driving our results, we would expect to see different effects of fiscal policy depending on political orientation. We repeat the same interaction procedures as described above for income, but replacing income with people’s political orientation. As can be seen from Figure 3, we find the same effect of fiscal policies for people of different political orientations: the slope estimates are smaller than for the income interactions and none are significant at the 5% level (though the interaction with distortionary taxation is significant at the 10% level), while the non-parametric fits reveal no discernible trend.

5.3 Regions: Heterogeneous settlement size and subnational effects

Our prior results all control for the settlement size of the individual respondent but do not allow the fiscal impacts to vary by settlement size, nor do they test whether national versus subnational fiscal policies have differential effects on SWB. In addition, fiscal policy may affect wealthier countries differently to less wealthy ones and this effect may differ by town size. Here we test each of these region-related aspects.

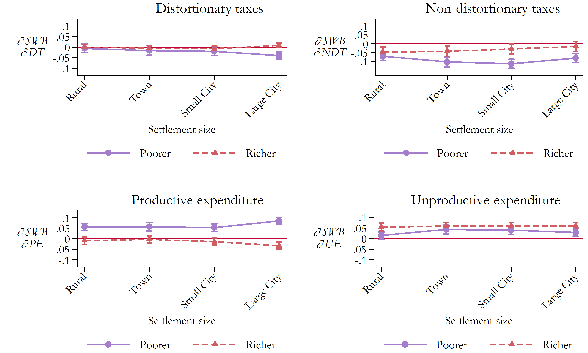

5.3.1 Settlement size and country income

We investigate whether fiscal policies affect people living in different sized towns and cities in different ways. To do so, we interact the size of a person’s settlement with the fiscal policy variables. We test whether these effects may differ according to the wealth of countries by creating a dummy variable (richer/poorer), which splits our sample roughly in half, based on 1990 GDP per capita (using PWT 8.1 definitions of GDP and population). We stress here that our sample does not include developing countries, and that generally the ‘poorer’ countries are at least middle income29 . We then interact our rich/poor variable with both fiscal policy and town size. This allows the effect of each fiscal variable to differ across the 8 different combinations of country wealth and town size.

The results (again using the central government definitions) are presented in Figure 4. (Linear interactions are not included given the non-linear definitions of settlement size in the data.)

Productive expenditure appears to be more beneficial for SWB in poorer countries, while there is some evidence that non-distortionary taxes are more detrimental in poorer countries. Distortionary taxation appears to have similar effects in both rich and poor countries. Unproductive expenditures have a similar effect on SWB in both rich and poor countries, with only weak evidence for more positive effects in richer countries.

Turning to differences in fiscal policy’s influence across town size (i.e. the slope of the lines in Figure 4) we find little variation, with the 90% confidence intervals largely overlapping. There is, perhaps, some evidence for differences in effects of distortionary taxes, and productive expenditure in cities with more than 100,000 people (‘large cities’), but care should be taken here for several reasons. Firstly, the results differ for wealthier and less wealthy countries; in richer countries the effects of productive expenditure deteriorate in the larger settlements, while in poorer countries the effects of productive expenditure improve in larger settlements. A priori, we have no strong reason to suppose this. Relatedly, given the multiple comparisons being made here, deviations like this may occur from chance alone (i.e. a false positive). Finally, the relative incomes of people within a country (rather than the across country differences) are correlated with settlement size, so it is possible that the estimated association found here is driven not by the size of the town per se but by the differences in incomes of the people living in these towns.

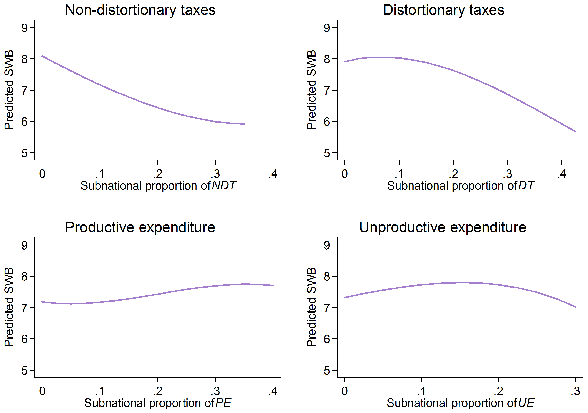

5.3.2 Devolution of fiscal policy to subnational government

We examine the relationship to wellbeing of differences in the degree to which fiscal expenditures and revenues are centralized or decentralized to subnational government. Subnational government is taken to comprise all levels of government below central government (i.e. including both state and municipal governments).

For each fiscal category, we calculated the proportion of general government taxation or

expenditure that occurs at the subnational level. The proportion that is subnational is defined

as 1 - , where varCG is the amount of the fiscal variable reported at the central

government level and varGG the amount reported at the general government level. We

investigated other definitions but consider this definition to be the most reliable of those

available. For example, we had measures of local and regional government fiscal variables from

an alternative data source, which we added to form an estimate of the subnational component,

varSN, allowing us to estimate the proportion subnational as

, where varCG is the amount of the fiscal variable reported at the central

government level and varGG the amount reported at the general government level. We

investigated other definitions but consider this definition to be the most reliable of those

available. For example, we had measures of local and regional government fiscal variables from

an alternative data source, which we added to form an estimate of the subnational component,

varSN, allowing us to estimate the proportion subnational as  for each

fiscal variable. Unfortunately, these estimates of subnational government were often

implausible (most probably due to double counting of taxes and expenditures in the

subnational categories) and, as a result, the corresponding results differ to those presented

below30 .

The measure of subnational government that we use has deficiencies as a result of

drawing data from different sources that may have slightly different fiscal definitions

to each other (and which could include some double counting), explaining why we

have isolated country examples where central government is greater than general

government within a particular fiscal category. For these reasons, while we have used

the best available data, our results in this section should be interpreted with some

caution.

for each

fiscal variable. Unfortunately, these estimates of subnational government were often

implausible (most probably due to double counting of taxes and expenditures in the

subnational categories) and, as a result, the corresponding results differ to those presented

below30 .

The measure of subnational government that we use has deficiencies as a result of

drawing data from different sources that may have slightly different fiscal definitions

to each other (and which could include some double counting), explaining why we

have isolated country examples where central government is greater than general

government within a particular fiscal category. For these reasons, while we have used

the best available data, our results in this section should be interpreted with some

caution.

We estimated Equation (6), being our baseline equation modified to include terms for the proportion of each variable that is subnational (denoted by the vector S). A non-linear relationship is implied if the optimal level of subnational government is neither 0% nor 100%. We find that a cubic specification best fits the data31 . Hence, our baseline estimation includes S2 and S3, vectors whose elements are the squares and cubes of the elements in S.

| (6) |

Figure 5 plots the predicted values from the regression in (6), as each subnational proportion variable is varied between 0 and its 90th percentile in the regression sample. For each plot, all other variables are evaluated at their sample means.

The results suggest that taxation is best done centrally, while expenditure is best done by a combination of central and subnational government. This is consistent with economies of scale being important for revenue raising, and with local knowledge being important for expenditure. In other words, it appears optimal to keep taxation systems simple and centralized, and to allow fiscal expenditures some latitude to reflect local complexities.

6 Conclusions

Economic growth is not an end in itself, but instead is a means to greater utility or wellbeing. While the empirical literature on the effects of fiscal policy has hitherto focussed on GDP growth, we have focused on subjective wellbeing – an important measure of people’s overall wellbeing. Our evidence on the relationships between fiscal policy and subjective wellbeing can feed into the decisions of policymakers who have policy goals that extend beyond economic growth.

The small amount of prior literature relating to fiscal policy and wellbeing has focused on the overall size of government, without addressing how government is financed. We adapt the methodology used in the (Bleaney et al. 2001) GDP growth study to explicitly control for the government budget constraint, estimating the relationship between wellbeing and taxation and expenditure shares. In line with the Barro endogenous growth framework and the approach taken by Bleaney, Gemmell and Kneller, we distinguish between the effects of four broad fiscal categories: “productive expenditure”, or government-provided capital; “unproductive expenditure”, or government-provided consumption; “distortionary taxation” such as income taxes and social security contributions; and “non-distortionary taxation” such as VAT. We retain their definitions of these variables to enable comparisons with the prior literature. This study is, to the best of our knowledge, the first in the SWB literature to explicitly consider the government budget constraint, the first to consider SWB within the context of endogenous growth theory, and the first to examine regional and subnational dimensions of the relationship of fiscal policies with subjective wellbeing.

We use fiscal data from the IMF Government Finance Statistics and the OECD, for 35 countries and 130 country-years. Unlike almost all previous studies, we make use of general government as well as central government data. We combine our fiscal data with over 170,000 individual responses from the World Values Survey and European Values Study and with macroeconomic data from various sources.

We find a number of important relationships, even after including country fixed effects and a suite of macroeconomic and personal controls. First, we find a positive association between SWB and a decrease in non-distortionary taxes funded by an increase in distortionary taxation. Second, we find a positive association between SWB and an increase in productive expenditures funded by a decrease in unproductive expenditures. While we find no material differences across the political spectrum, we do find differences in associations across people of different incomes: Richer people are hurt more by distortionary taxation and less by non-distortionary taxation than poorer people. They also benefit by less than poorer people do from productive expenditures. The middle class appear to benefit the most from unproductive expenditures, consistent with a theory of middle class capture.

In examining regional issues, we find no material differences in the effects of fiscal policy across people living in different-sized settlements. However, we do uncover important patterns related to subnational versus central government fiscal policies. Most notably, we find a positive association, up to a point, between SWB and an increase in the share of expenditures that are spent subnationally. Additionally, we find a negative association between SWB and an increase in the share of tax revenue raised subnationally. Thus our findings support taxation being a central government function while fiscal expenditures appear to be best provided by a combination of central and subnational governments.

Our estimates control for personal characteristics of the over 170,000 individuals in our sample and control for a suite of macroeconomic circumstances that could independently affect wellbeing. We see no strong reason to expect material reverse causality from subjective wellbeing to fiscal policies or to expect any major sources of omitted variables bias, especially given that we have controlled for macroeconomic conditions. Nevertheless, future research could further examine the extent to which the relationships that we establish are causal and examine the causal pathways through which these relationships act. In particular, our findings regarding the optimal roles for subnational versus central government fiscal policies could prove a fruitful area for further research with an emphasis on uncovering particular categories of expenditures (and taxes) that are best retained at the central government level and those that are best devolved to subnational government.

References

Alesina A, Rodrik D (1994) Distributive politics and economic growth. The Quarterly Journal of Economics 109: 465–490. CrossRef.

Angelopoulos K, Economides G, Kammas P (2007) Tax-spending policies and economic growth: Theoretical predictions and evidence from the oecd. European Journal of Political Economy 23: 885–902. CrossRef.

Angrist JD, Pischke JS (2008) Mostly Harmless Econometrics: An Empiricist’s Companion. Princeton University Press, Princeton

Baier SL, Glomm G (2001) Long-run growth and welfare effects of public policies with distortionary taxation. Journal of Economic Dynamics and Control 25: 2007–2042. CrossRef.

Barro RJ (1990) Government spending in a simple model of endogeneous growth. Journal of Political Economy 98: S103–S125. CrossRef.

Barro RJ, Sala-i Martin X (1992) Public finance in models of economic growth. The Review of Economic Studies 59: 645–661. CrossRef.

Berry BJL, Okulicz-Kozaryn A (2009) Dissatisfaction with city life: A new look at some old questions. Cities 26: 117–124. CrossRef.

Berry BJL, Okulicz-Kozaryn A (2011) An urban-rural happiness gradient. Urban Geography 32: 871–883. CrossRef.

Bjørnskov C, Dreher A, Fischer JAV (2007) The bigger the better? Evidence of the effect of government size on life satisfaction around the world. Public Choice 130: 267–292. CrossRef.

Black D (1948) On the rationale of group decision-making. Journal of Political Economy 56: 23–34. CrossRef.

Bleaney M, Gemmell N, Kneller R (2001) Testing the endogenous growth model: Public expenditure, taxation, and growth over the long run. Canadian Journal of Economics 34: 36–57. CrossRef.

Bowen HR (1943) The interpretation of voting in the allocation of economic resources. The Quarterly Journal of Economics 58: 27–48. CrossRef.

Case A, Deaton A (2015) Suicide, age, and wellbeing: An empirical investigation. Working paper 21279. National Bureau of Economic Research. http://www.nber.org/papers/w21279. CrossRef.

Clark AE, Diener E, Georgellis Y, Lucas RE (2008) Lags and leads in life satisfaction: A test of the baseline hypothesis. Economic Journal 118: F222–F243. CrossRef.

Daly MC, Wilson DJ (2009) Happiness, unhappiness, and suicide: An empirical assessment. Journal of the European Economic Association 7: 539–549. CrossRef.

Daly MC, Wilson DJ, Johnson NJ (2013) Relative status and well-being: Evidence from us suicide deaths. Review of Economics and Statistics 95: 1480–1500. CrossRef.

Di Tella R, MacCulloch RJ, Oswald AJ (2003) The macroeconomics of happiness. Review of Economics and Statistics 85: 809–827. CrossRef.

Diener E, Chan MY (2011) Happy people live longer: Subjective well-being contributes to health and longevity. Applied Psychology: Health and Well-Being 3: 1–43. CrossRef.

Diener E, Inglehart R, Tay L (2013) Theory and validity of life satisfaction scales. Social Indicators Research 112: 497–527. CrossRef.

Donnelly M, Pop-Eleches G (2012) The questionable validity of income measures in the world values survey. prepared for the princeton university political methodology seminar. http://www.princeton.edu/politics/about/filerepositpry/public/DonnellyPopElechesMarch16.pdf

Easterlin RA (1974) Does economic growth improve the human lot? In: David PA, Reder MW (eds), Nations and Households in Economic Growth: Essays in Honor of Moses Abramovitz. Academic Press, New York, 89–125

Easterlin RA, Angelescu L, Zweig JS (2011) The impact of modern economic growth on urban-rural differences in subjective well-being. World Development 39: 2187–2198. CrossRef.

Easterlin RA, Angelescu McVey L, Switek M, Sawangfa O, Zweig JS (2010) The happiness–income paradox revisited. Proceedings of the National Academy of Sciences 107: 22463–22468. CrossRef.

European Commission (2015) Economic and financial affairs. http://ec.europa.eu/economy\_finance/ameco/user/serie/SelectSerie.cfm

EVS – European Values Study (2011) European values study longitudinal data file 1981-2008. Za4804 version 2.0.0. cologne: Gesis. https://dbk.gesis.org/dbksearch/sdesc2.asp?.no=4804\&db=e\&doi=10.4232/1.11005

Feenstra RC, Inklaar R, Timmer MP (2015) The next generation of the Penn World Table. American Economic Review 105: 3150–3182. CrossRef.

Flavin P, Pacek AC, Radcliff B (2011) State intervention and subjective well-being in advanced industrial democracies. Politics & Policy 39: 251–269

Flavin P, Pacek AC, Radcliff B (2014) Assessing the impact of the size and scope of government on human well-being. Social Forces 92: 1241–1258. CrossRef.

Futagami K, Shibata A, Morita Y (1993) Dynamic analysis of an endogenous growth model with public capital. The Scandinavian Journal of Economics 95: 607–625. CrossRef.

Grimes A, Reinhardt MG (2015) Relative income and subjective wellbeing: Intra-national and inter-national comparisons by settlement and country type. Working paper 15-10, Motu Economic and Public Policy Research

Helliwell JF (2007) Well-being and social capital: Does suicide pose a puzzle? Social Indicators Research 81: 455–496. CrossRef.

Helliwell JF, Huang H (2008) How’s your government? international evidence linking good government and well-being. British Journal of Political Science 38: 595–619. CrossRef.

Helliwell JF, Layard R, Sachs J (2012) World happiness report 2012. http://worldhappiness.report/wp-content/uploads/sites/2/2012/04/World_Happiness_Report_2012.pdf

Hessami Z (2010) The size and composition of government spending in europe and its impact on well-being. Kyklos 63: 346–382. CrossRef.

Hotelling H (1929) Stability in competition. The Economic Journal 39: 41–57. CrossRef.

IMF – International, Monetary Fund (2014) Government finance statistics. http://www.imf.org/external/Pubs/FT/GFS/Manual/2014/gfsfinal.pdf

Kneller R, Bleaney MF, Gemmell N (1999) Fiscal policy and growth: Evidence from oecd countries. Journal of Public Economics 74: 171–190. CrossRef.

Layard R (2005) Happiness: Lessons Form a New Science. Allen Lane, London

Lucas RE (1988) On the mechanics of economic development. Journal of Monetary Economics 22: 3–42. CrossRef.

Misch F, Gemmell N, Kneller R (2013) Growth and welfare maximization in models of public finance and endogenous growth. Journal of Public Economic Theory 15: 939–967. CrossRef.

Morrison PS (2011) Local expressions of subjective well-being: The New Zealand experience. Regional Studies 45: 1039–1058. CrossRef.

Nijkamp P, Poot J (2004) Meta-analysis of the effect of fiscal policies on long-run growth. European Journal of Political Economy 20: 91–124. CrossRef.

OECD (2014) OECD government finance statistics. http://www.oecd-ilibrary.org/economics/data/general-government-accounts_na-gga-data-en

Oishi S, Schimmack U, Diener E (2011) Progressive taxation and the subjective well-being of nations. Psychological Science 23: 86–92. CrossRef.

Ram R (2009) Government spending and happiness of the population: Additional evidence from large cross-country samples. Public Choice 138: 483–490. CrossRef.

Rebelo S (1991) Long-run policy analysis and long-run growth. The Journal of Political Economy 99: 500–521. CrossRef.

Romer PM (1986) Increasing returns and long-run growth. The Journal of Political Economy 94: 1002–1037. CrossRef.

Romer PM (1988) Capital accumulation in the theory of long run growth. University of Rochester-Center for Economic Research (RCER). http://ideas.repec.org/p/roc/rocher/123.html

Schwarz N (1987) Stimmung als Information: Untersuchungen zum Einfluss von Stimmungen auf die Bewertung des eigenen Lebens. Springer Verlag, Heidelberg. CrossRef.

Stevenson B, Wolfers J (2008) Economic growth and subjective well-being: Reassessing the Easterlin Paradox. National Bureau of Economic Research, http://www.nber.org/papers/w14282. CrossRef.

Stiglitz JE (1988) Economics of the Public Sector (Second ed.). W W Norton & Company Inc, New York

The United Nations (2015) UN data. http://data.un.org/

The World Bank (2015a) Consumer price index for Argentina. FRED, Federal Reserve Bank of St. Louis, https://research.stlouisfed.org/fred2/series/DDOE01ARA086NWDB/

The World Bank (2015b) World bank development indicators 2014. The World Bank, http://data.worldbank.org/indicator/NE.GDI.TOTL.ZS

The World Bank (2015c) World bank development indicators 2015. The World Bank

Turnovsky SJ (2000) Fiscal policy, elastic labor supply, and endogenous growth. Journal of Monetary Economics 45: 185–210. CrossRef.

Urry HL, Nitschke JB, Dolski I, Jackson DC, Dalton KM, Mueller CJ, Rosenkranz MA, Ryff CD, Singer BH, Davidson RJ (2004) Making a life worth living. Neural correlates of well-being. Psychological Science 15: 367–372. CrossRef.

Veenhoven R (1994) How satisfying is rural life? fact and value. In: Cecora J (ed), Changing Values and Attitudes in Family Households, Implications for Institutional Transition in East and West. Society for agricultural policy research in rural society, Bonn, Germany, 41–51

Veenhoven R (2000) Well-being in the welfare state: Level not higher, distribution not more equitable. Journal of Comparative Policy Analysis: Research and Practice 2: 91–125. CrossRef.

WVSA – World Values Survey Association (2014) World values survey 1981-2014 longitudinal aggregate v.20141125. http://www.worldvaluessurvey.org

A Appendix

A.1 Data

We cleaned the IMF and OECD fiscal data to remove unreliable observations. We explain the most important parts of this cleaning here. Full detail can be found in our code which we have placed on the Motu website (www.motu.org.nz).

A.1.1 Modern vs. Historical GFS

The IMF data from 1972 – 1989 is classified using the ‘historical’ 1986 definitions while the data from 1990 onwards are classified using the ‘modern’ 2001 format. We followed the IMF’s guidelines for reclassifying data from 1986 to 2001 format. The key differences between the historical and modern format is that the historical outlays include gross purchases of capital assets in the relevant COFOG category, while modern only reports net purchases of capital in the functional categories. There is no way to convert 1986 expenditure data exactly to the 2001 definition because there is no information to allocate sales of capital assets to the various functions. There are also issues with how revenues of government enterprises and social contributions for government employees are reported. Finally environmental protection is a new category in GFS2001.

In addition the modern IMF GFS statistics include both accrual and cash based definitions of fiscal variables – with neither versions of the variables offering complete coverage. For this reason we use the cash data where possible, and then for the remainder we use the accrual data – modified to be more comparable to the cash data. The modification process is as follows: first we look at cases where we have both the accrual and cash data. Then we calculate the 10% trimmed mean of the ratio of cash to accrual (separately for each variable). Finally the accrual data is multiplied by this (variable specific) ratio.

The OECD data and IMF fiscal data appear to be compiled differently. To make them comparable we use the same method as we did for converting accrual to cash data.

A.1.2 Dropping of countries with unreliable data

We inspected the fiscal data for all countries in our analysis. Where the data looked unreliable that country was dropped – at least for the period where the data looked unstable. In particular we included most countries where none of their key fiscal variables changed by more than 7 percentage points since last observed (usually the previous year). For countries that had changes larger than 7 percentage points we inspected to see if these changes plausibly reflected real changes rather than just questionable data. For example, our data showed Iceland’s unproductive expenditures increased by over 10 percentage points of GDP in 2008, but given their massive banking failure that year, such variation is to be expected, and so Iceland is included in our analysis. On the hand, the 15 percentage point increase in NZ productive expenditure as a share of GDP from 2007 to 2009 is judged to be inaccurate data, and so New Zealand is excluded from our analysis. We limit our focus to high and middle income countries excluding low income countries such as India.

A.2 Tables and Figures

| Symbol | THEORETICAL CATEGORY | IMF FUNCTIONAL CATEGORY |

|

DT |

Distortionary taxation | Taxation on income and profit |

| Social security contributions | ||

| Taxation on payroll and manpower | ||

| Taxation on property | ||

| NDT | Non-distortionary taxation | Taxes on goods and services |

|

PE |

Productive expenditures | General public services |

| Defence | ||

| Education | ||

| Health | ||

| Housing | ||

| Transport and communication | ||

|

UE |

Unproductive expenditures | Social security and welfare |

| Recreation | ||

| Economic services | ||

| OR | Other revenues | |

| OE | Other expenditure | |

| BS | Budget surplus | We define this as the residual: |

| DTt + NDTt + ORt - PEt- | ||

| UEt - OEt ≡ BSt | ||

| Number | ||||||

| Mean | Median | s.d | Min | Max | country-year | |

| obs | ||||||

| Distortionary taxation | 24.91 | 24.8 | 5.92 | 7.36 | 37.62 | 79 |

| Non-distortionary taxation | 10.74 | 11.26 | 2.73 | 4.01 | 15.91 | 79 |

| Productive expenditures | 21.6 | 22.07 | 3.58 | 10.37 | 29.79 | 79 |

| Unproductive expenditures | 19.39 | 19.94 | 4.88 | 3.09 | 29.44 | 79 |

| Other revenues | 7.05 | 6.62 | 2.79 | 3.54 | 18.37 | 79 |

| Other expenditures | 0.12 | 0.08 | 0.49 | -0.62 | 3.32 | 79 |

| Distortionary taxation | 18.46 | 19.06 | 6.05 | 4.3 | 32.1 | 129 |

| Non-distortionary taxation | 9.58 | 10.58 | 3.79 | 0.61 | 18.74 | 129 |

| Productive expenditures | 17.14 | 16.65 | 4.85 | 5.05 | 28.47 | 129 |

| Unproductive expenditures | 17.04 | 17.38 | 5.23 | 3.09 | 31.16 | 129 |

| Other revenues | 4.63 | 4.16 | 2.9 | 1.36 | 23.12 | 129 |

| Other expenditures | -0.12 | 0 | 0.95 | -6.11 | 2.01 | 129 |

| Inflation (% p.a.) | 5.87 | 3.27 | 9.14 | -1.82 | 83.99 | 129 |

| Investment | 23.48 | 23.42 | 3.64 | 14.64 | 32.69 | 128 |

| Unemployment (% p.a.) | 7.58 | 7.1 | 3.73 | 1.7 | 21.4 | 127 |

| Proportion of fiscal variable that | ||||||

| is subnational government*** | ||||||

| Non-distortionary taxation | 0.12 | 0.05 | 0.17 | -0.05 | 0.62 | 69 |

| Distortionary taxation | 0.19 | 0.15 | 0.16 | 0 | 0.54 | 69 |

| Productive expenditures | 0.15 | 0.13 | 0.18 | -0.18 | 0.64 | 69 |

| Unproductive expenditures | 0.13 | 0.13 | 0.14 | -0.31 | 0.42 | 69 |

Notes: The fiscal variables (first two panels) are expressed as a percentage of GDP. Investment is also expressed as a percentage of GDP. All figures rounded to 2 d.p. Figures are based on the country-years that are included in (certain) regressions. * Based on general government sample. ** Based on central government sample. *** Based on proportion government sample.

| mean | median | sd | min | max | N | |

| Subjective wellbeing | ||||||

| SWB - Central government sample | 7.26 | 8 | 2.05 | 1 | 10 | 110,659

|

| SWB - General government sample | 7.26 | 8 | 2.07 | 1 | 10 | 171,804

|

| SWB - Proportion subnational sample | 7.33 | 8 | 1.98 | 1 | 10 | 93,280

|

| Income scale | ||||||

| Income - Central government sample | 4.83 | 5 | 2.43 | 1 | 10 | 65,595

|

| Income - General government sample | 5.03 | 5 | 2.53 | 1 | 10 | 110,780

|

| Income - Proportion subnational sample | 4.87 | 5 | 2.39 | 1 | 10 | 51,416

|

| Political scale - 1 = left ;10 = right | ||||||

| Political scale - Central government sample | 5.31 | 5 | 2.08 | 1 | 10 | 89,527

|

| Political scale - General government sample | 5.38 | 5 | 2.06 | 1 | 10 | 137,087

|

| Political scale - Proportion subnational sample | 5.27 | 5 | 2.03 | 1 | 10 | 74,624

|

| Gender | ||||||

| Female - Central government sample | 0.54 | 1 | 0.50 | 0 | 1 | 110,617

|

| Female - General government sample | 0.54 | 1 | 0.50 | 0 | 1 | 171,696

|

| Female - Proportion subnational sample | 0.54 | 1 | 0.50 | 0 | 1 | 93,240

|

| EVS vs. WVS | ||||||

| WVS - Central government sample | 0.51 | 1 | 0.50 | 0 | 1 | 110,659

|

| WVS - General government sample | 0.44 | 0 | 0.50 | 0 | 1 | 171,804

|

| WVS - Proportion subnational sample | 0.43 | 0 | 0.50 | 0 | 1 | 93,280

|

| Age | ||||||

| Age - Central government sample | 46.52 | 45 | 17.65 | 15 | 108 | 110,378

|

| Age - General government sample | 45.56 | 44 | 17.71 | 14 | 108 | 169,876

|

| Age – Proportion subnational sample | 46.94 | 46 | 17.76 | 15 | 108 | 93,020

|

Note: Education, and settlement size are also included as controls in our regressions, though (because they are categorical and cumbersome to summarize) they are not included in this table. Age is summarised here as a continuous variable but included in bins in the analysis (see Section 3.2 for details). The N in the last column refers to the number of non-missing observations for that variable, but people with missing values for these personal controls are included in the analysis (with separate missing categories for each variable, again refer to Section 3.2 for more detail).

| Country | Central government | General government | Subnational proportion |

| regression | regression | regression | |

| Australia | 1 | 1 | 1 |

| Austria | 1 | 1 | 1 |

| Belgium | 1 | 1 | 1 |

| Canada | 1 | 1 | 1 |

| Denmark | 1 | 1 | 1 |

| Estonia | 1 | 1 | 1 |

| Finland | 1 | 1 | 1 |

| France | 1 | 1 | 1 |

| Germany | 1 | 1 | 1 |

| Great Britain | 1 | 1 | 1 |

| Greece | 1 | 1 | 1 |

| Hungary | 1 | 1 | 1 |

| Iceland | 1 | 1 | 1 |

| Italy | 1 | 1 | 1 |

| Luxembourg | 1 | 1 | 1 |

| Malta | 1 | 1 | 1 |

| Netherlands | 1 | 1 | 1 |

| Norway | 1 | 1 | 1 |

| Poland | 1 | 1 | 1 |

| Portugal | 1 | 1 | 1 |

| Singapore | 1 | 1 | 1 |

| Slovenia | 1 | 1 | 1 |

| Spain | 1 | 1 | 1 |

| Sweden | 1 | 1 | 1 |

| Switzerland | 1 | 1 | 1 |

| Cyprus (T) | 1 | 1 | 0 |

| Japan | 1 | 1 | 0 |

| United States | 1 | 1 | 0 |

| South Africa | 0 | 1 | 0 |

| Argentina | 1 | 0 | 0 |

| Chile | 1 | 0 | 0 |

| Czech Rep. | 1 | 0 | 0 |

| Ireland | 1 | 0 | 0 |

| Lithuania | 1 | 0 | 0 |

| Ukraine | 1 | 0 | 0 |

| Fiscal definition: | Central | Central | General | General

| ||||

| Government | Government | Government | Government

| |||||

| Non-distortionary taxes GG | -0. | 057*** | -0. | 100*** | ||||

| (0. | 012) | (0. | 014) | |||||

| Distortionary taxes GG | -0. | 002 | -0. | 005 | ||||

| (0. | 007) | (0. | 007) | |||||

| Productive exp. GG | 0. | 025*** | 0. | 046*** | ||||

| (0. | 007) | (0. | 008) | |||||

| Unproductive exp.GG | 0. | 016** | 0. | 006 | ||||

| (0. | 008) | (0. | 01) | |||||

| Other rev. GG | 0. | 039*** | 0. | 028** | ||||

| (0. | 01) | (0. | 011) | |||||

| Other exp. GG | 0. | 156*** | 0. | 159*** | ||||

| (0. | 023) | (0. | 024) | |||||

| Non-distortionary taxes CG | -0. | 045*** | -0. | 045*** | ||||

| (0. | 007) | (0. | 007) | |||||

| Distortionary taxes CG | 0. | 005* | -0. | 002 | ||||

| (0. | 003) | (0. | 003) | |||||

| Productive exp. CG | 0. | 043*** | 0. | 048*** | ||||

| (0. | 003) | (0. | 003) | |||||

| Unproductive exp. CG | 0. | 001 | 0. | 015*** | ||||

| (0. | 004) | (0. | 004) | |||||

| Other rev. CG | -0. | 005 | -0. | 010* | ||||

| (0. | 005) | (0. | 006) | |||||

| Other exp. CG | 0. | 009 | 0. | 021** | ||||

| (0. | 008) | (0. | 008) | |||||

| ln_gdppc | 1. | 041*** | 1. | 260*** | 0. | 758*** | 0. | 635*** |

| (0. | 066) | (0. | 115) | (0. | 14) | (0. | 237) | |

| ln_gdppc (t - 3) | -0. | 405*** | -0. | 026 | ||||

| (0. | 091) | (0. | 24) | |||||

| inflation | 0. | 002 | -0. | 052*** | ||||

| (0. | 001) | (0. | 007) | |||||

| investment | 0. | 008** | 0. | 036*** | ||||

| (0. | 003) | (0. | 006) | |||||

| unemployment | -0. | 007* | 0. | 007 | ||||

| (0. | 003) | (0. | 006) | |||||

| N | 171,804 | 169,900 | 110,659 | 110,659

| ||||

| No. of countries | 34 | 34 | 29 | 29

| ||||

| No. of country-time obs. | 129 | 127 | 79 | 79

| ||||

| Personal controls | YES | YES | YES | YES

| ||||

| Survey wave fixed effects | YES | YES | YES | YES

| ||||

| Country fixed effects | YES | YES | YES | YES

| ||||

| R squared | 0. | 122 | 0. | 124 | 0. | 113 | 0. | 114 |

Notes: Robust standard errors in parentheses. Omitted fiscal category is the budget surplus, and hence the statistical significance reported by the stars refer to statistical difference from the surplus. Dependent variable is an individual’s subjective wellbeing in all regressions. ln_gdppc is the natural log of GDP per capita. ln_gdppc (t - 3) is the natural log of GDP per capita 3 years ago. Personal controls are: age, education, gender, income (as a scale), political orientation, a dummy for survey type, and settlement size (see section 3.2 and Table A.3 for more details on these). Stars denote: * p<0.10, ** p<0.05, *** p<0.01

| (1) | (3) | (3)

| ||||

| Non-distortionary taxes GG | -0. | 166*** | -0. | 143*** | -0. | 140*** |

| (0. | 021) | (0. | 022) | (0. | 024) | |

| Distortionary taxes GG | 0. | 023** | 0. | 031*** | 0. | 038*** |

| (0. | 010) | (0. | 010) | (0. | 012) | |

| Productive exp. GG | 0. | 041*** | 0. | 021** | 0. | 018 |

| (0. | 010) | (0. | 010) | (0. | 011) | |

| Unproductive exp.GG | 0. | 005 | 0. | 047*** | 0. | 037** |

| (0. | 013) | (0. | 015) | (0. | 017) | |

| Other rev. GG | 0. | 030* | 0. | 090*** | 0. | 082*** |

| (0. | 016) | (0. | 019) | (0. | 020) | |

| Other exp. GG | 0. | 258** | 0. | 285** | 0. | 291** |

| (0. | 114) | (0. | 116) | (0. | 124) | |

| subnational proportion of NDT | -1. | 148*** | -6. | 275*** | -9. | 737*** |

| (0. | 304) | (0. | 870) | (1. | 520) | |

| (subnational proportion of NDT)**2 | 8. | 768*** | 4. | 038 | ||

| (1. | 256) | (7. | 152) | |||

| (subnational proportion of NDT)**3 | 17. | 348* | ||||

| (9. | 214) | |||||

| subnational proportion of DT | 0. | 535 | 0. | 695 | 4. | 413* |

| (0. | 518) | (1. | 138) | (2. | 273) | |

| (subnational proportion of DT)**2 | -3. | 905** | -34. | 953*** | ||

| (1. | 785) | (8. | 923) | |||

| (subnational proportion of DT)**3 | 28. | 685*** | ||||

| (10. | 326) | |||||

| subnational proportion of PE | 0. | 195 | -1. | 040** | -2. | 362*** |

| (0. | 368) | (0. | 490) | (0. | 522) | |

| (subnational proportion of PE)**2 | 0. | 187 | 26. | 730*** | ||

| (1. | 418) | (3. | 504) | |||

| (subnational proportion of PE)**3 | -43. | 822*** | ||||

| (5. | 347) | |||||

| subnational proportion of UE | -0. | 77 | -0. | 291 | 5. | 118*** |

| (0. | 487) | (0. | 551) | (0. | 953) | |

| (subnational proportion of UE)**2 | -4. | 346** | -5. | 275*** | ||

| (1. | 766) | (2. | 041) | |||

| (subnational proportion of UE)**3 | -50. | 205*** | ||||

| (7. | 628) | |||||

| N | 93,280 | 93,280 | 93,280

| |||

| No. of countries | 25 | 25 | 25

| |||

| No. of country-time obs. | 69 | 69 | 69

| |||

| Macro controls | YES | YES | YES

| |||

| Personal controls | YES | YES | YES

| |||

| Survey wave fixed effects | YES | YES | YES

| |||

| Country fixed effects | YES | YES | YES

| |||

| R squared | 0. | 103 | 0. | 104 | 0. | 105 |

| Adjusted R squared | 0. | 102 | 0. | 103 | 0. | 104 |

| Akaike information criterion | 382,521 | 382,479 | 382,400

| |||

| Bayesian information criterion | 383,342 | 383,338 | 383,297

| |||

See notes to Table A.5.